Disney Bucks Market Trend And Rises To New All-Time Highs

After hitting all-time highs in mid-February, the broader markets have begun to sell-off a bit during recent trading sessions, due primarily to fears surrounding rising interest rates. During the last week, the Dow Jones Industrial Average (DJI) has traded relatively flatly, and sits just just a few tenths of a percent below its record highs. However, the S&P 500 (SPY) is down roughly 1.5% during the past 5 trading sessions and the more growth oriented and technology heavy NASDAQ 100 Index (QQQ) is down roughly 4.2%.

Many of the market’s top performers over the last several years are sought after growth stocks, yet these are precisely the names that are experiencing the most weakness right now because during a rising rate environment, stocks with higher price-to-earnings multiples are likely to suffer as the market re-prices risk and valuations contract.

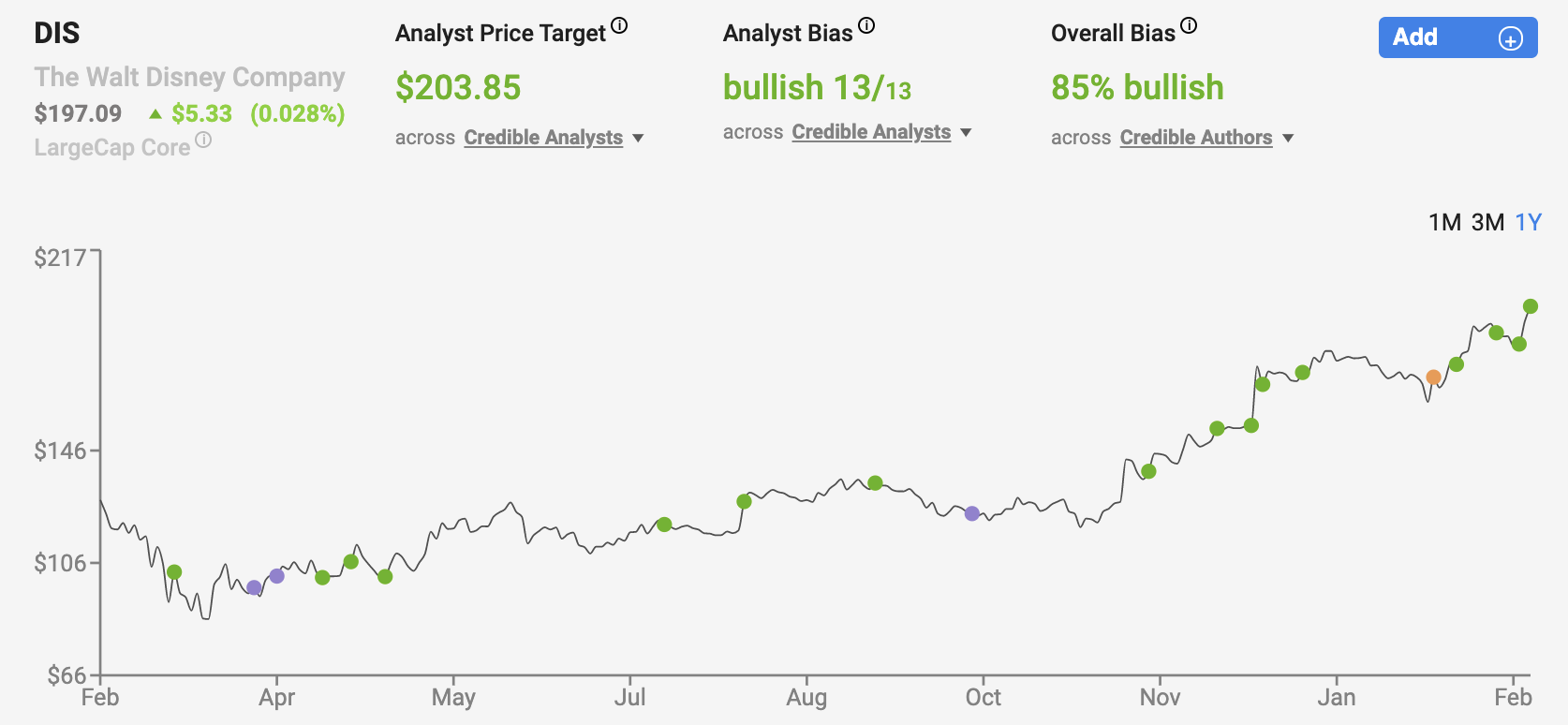

Yet, in recent weeks, Disney (DIS) shares have bucked this trend and continue to trade higher while so many of the high flyers from the past 12 months have sold off. During the past week, Disney shares are up 5.76%, having hit all-time highs yet again on Tuesday. Year-to-date, Disney shares are up 8.78%. And, during the trailing twelve months, Disney shares have risen 41.82%, which is more than twice as much as the S&P 500, which is up 16.06% during the same period of time.

Although Disney hasn’t always been thought of as a growth stock by the market, it is receiving growth stock treatment by investors today because of the tremendous success of its Disney+ streaming platform. Disney shares currently trade for $197.09, which results in a blended price-to-earnings ratio of 97.96x. For comparison’s sake, this is higher than the 82.28x blended multiple that Disney’s streaming rival Netflix (NFLX) currently carries.

Disney’s share price appreciation during the COVID-19 pandemic period has led to an unprecedented valuation for the stock. Disney’s 5, 10, and 20-year average price-to-earnings ratios are 18.8x, 18.35x, and 21.5x. It’s clear that investors buying Disney shares at all-time highs here with nose-bleed multiples attached to them are placing confident bets on the long-term future of the company.

Yet, when looking at recent reports from the 5-star analysts that Nobias tracks, it becomes clear why there is such strong bullish sentiment behind Disney stock. Jason Hall, contributor at The Motley Fool, put it simply in a recent podcast, saying, “I've called Disney the best combination of a stay-at-home stock in a reopening stock all in one.”

Disney’s ability to satisfy the appetite of investors who’re looking for the strong performance of a “stay at home” stock and the strong upside potential of a “reopening” play puts it in rarified air (usually, these two investment theses are counter intuitive).

Sydnee Gateman of Gurufocus recently reported that the Yachtman Fund presented a very similar outlook in its recent shareholder letter, saying, “We believe the prospect of a recovery in the core businesses, combined with the growth of Disney+, positions the company well for the future.”

Joe Tenebruso, of The Motley Fool, agrees, having published an article titled on February 22, titled “Why Disney Stock Rose To An All-Time High Today”. In his article, Tenebruso comes to a similar conclusion as Hall and the Yacktman Fund, saying, “Its theme parks, cruise ships, and movie studios could see their revenues quickly rebound if the travel and entertainment industries experience a post-COVID boom. Meanwhile, its incredibly popular Disney+ streaming service will likely continue to fuel its growth during the remainder of the pandemic and in the years that follow.” Tenebruso concluded his piece, saying, “Investors seeking a relatively low-risk way to profit from an eventual return to normalcy would be wise to consider Disney.”

Disney+ Remains The Backbone Of Bullish Opinions

A common theme that we’re seeing here is a bullish focus on Disney+. The rise of Disney’s direct-to-consumer platform during the COVID-19 pandemic period has blown away analysts estimates and even Disney’s own internal projections. And, the pace of growth remains robust as Disney management has begun targeting international markets for future growth.

During Disney’s recent fourth quarter conference call, CEO Bob Chapek said that “Disney+ has exceeded even our highest expectations.” This isn’t an overstatement. During Disney’s 2019 Investor Day presentation, which was largely focused on the November 2019 launch of the Disney+ service, the Walt Disney Corporation projected that by the end of 2024, it would have 60-90 million paying customers. At the end of Q4 2020, Disney+ had 94.9 million subscribers.

Luke Lango, InvestorPlace Senior Investment Analyst, noted in a recent report that the Disney+ service “added 21.2 million subscribers in the quarter.” He continued, saying, “For comparison, over the roughly same time period, Netflix added about a third that at just 8.5 million subs.” Lango took a step back and looked at the year-long data as well, painting Disney in a bullish light as well, saying “Disney+ now has 94.9 million subscribers. The service started in November 2019. Thus, in just over a year, Disney+ has added about 100 million subscribers. Again, for comparison purposes, it took Netflix just over three years to add its latest batch of 100 million subs.” Noting that Disney’s average-revenue-per-user (ARPU) fell by 28% during the company’s most recent quarter as the company focused its investments and subscriber growth efforts in international markets, such as India; he concludes that “this is the right long-term strategy.” While he likes the company’s strategy to “Sign subscribers up with bargain pricing. Hook them with compelling content. Get them to stick as you gradually hike prices over time.”,

Lango also made a counterpoint to one of the most common bearish theses that surrounds Disney shares, relating to the cord-cutting phenomena that we’ve seen play out in recent years and suggestions that traditional, linear television as we know it, is dying out. Lango admits that this may be true; yet, he doesn’t believe this is necessarily a bad thing for Disney. He says, “While viewers’ watching habits will shift over the next decade from linear TV to streaming TV, what those viewers watch will not change. That is, in 2030, we will all just be streaming The Bachelor and NBA games.” He calls the transition from linear to streaming distribution networks a “no-loss” transition for Disney and believes that the companies who own the most thrilling content in the future will be the likely winners of the battle for market share that we’ve seen play out in recent years in the media space.

Park Struggles Won’t Last

While it’s true that Disney’s parks, resorts, cruise lines, and box office sales have suffered significant losses during the pandemic period (during the fourth quarter, Disney’s “Parks, Experiences, and Products” division, which is traditional very profitable, posted a net loss of $119 million), the 5-star analysts that we track don’t believe this will be a long lasting phenomena. Lango notes that “there is now a visible pathway towards 80%-plus global vaccination within the next 12 months” and therefore, “there is also a visible pathway towards Disney’s parks reopening without many restrictions within the next 12 months.”

The Motley Fool’s Matthew Frankel recently said that after “accelerated adoption” of the Disney+ platform, Disney is “Going to come out of this pandemic with this new multi-billion-dollar revenue stream they didn't have before, and demand for their legacy products if you can even call them that, are going to be just as strong as ever.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Frankel continues his bullish assessment, saying, “The bottom line is, I think Disney for me, it's like it's a own-it-for-a-century. This is a company that you leave to your heirs because they own the content and they own the most timeless content. People are going to be paying to watch The Avengers, people are going to be paying to watch Star Wars, they're going to be paying to watch all of the Disney-branded content a century from now, whatever medium it's being produced on.”

Analyst Price Targets Point Towards More Upside Head

This double edged sword, regarding the secular growth prospects of Disney+ in the digital streaming space and the “re-opening” rebound play that the parks/resorts is why Disney is exactly why demand for Disney shares remains high in a market where other, recent winners, are struggling.

And, with the average price target for Disney shares from amongst the 4 and 5-star analysts that Nobias tracks coming out to $222.50/share, which represents upside potential of 12.89% from today’s all-time high share prices, it appears as if this stock has more room to run.

Disclosure: Nicholas Ward is long Disney. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.