Micron: Analysts Believe That This Volatile Stock is Heading Higher

In early 2021, we saw frantic buying in the technology sector, especially amongst very speculative, high growth potential names, with little to no earnings power to speak of. These types of investments can be exciting; however, when investors are placing bets based upon double digit price-to-sales multiples, a lot has to go right over the long-term for such stocks to make sense, fundamentally.

That trade, which appears to have been largely fueled by retail investors attempting to “yolo” (you only live once) into get-rich-quick schemes has died off a bit over recent months however, and now, the market’s sentiment seems to be more positive towards stocks with strong cash flows and attractive earnings.

And, with that in mind, we’ve seen a strong uptick in articles and analyst opinions offered on a relatively cheap semiconductor stock which just posted strong earnings and appears to have a very attractive growth runway ahead of it. We’re talking about Micron (MU).

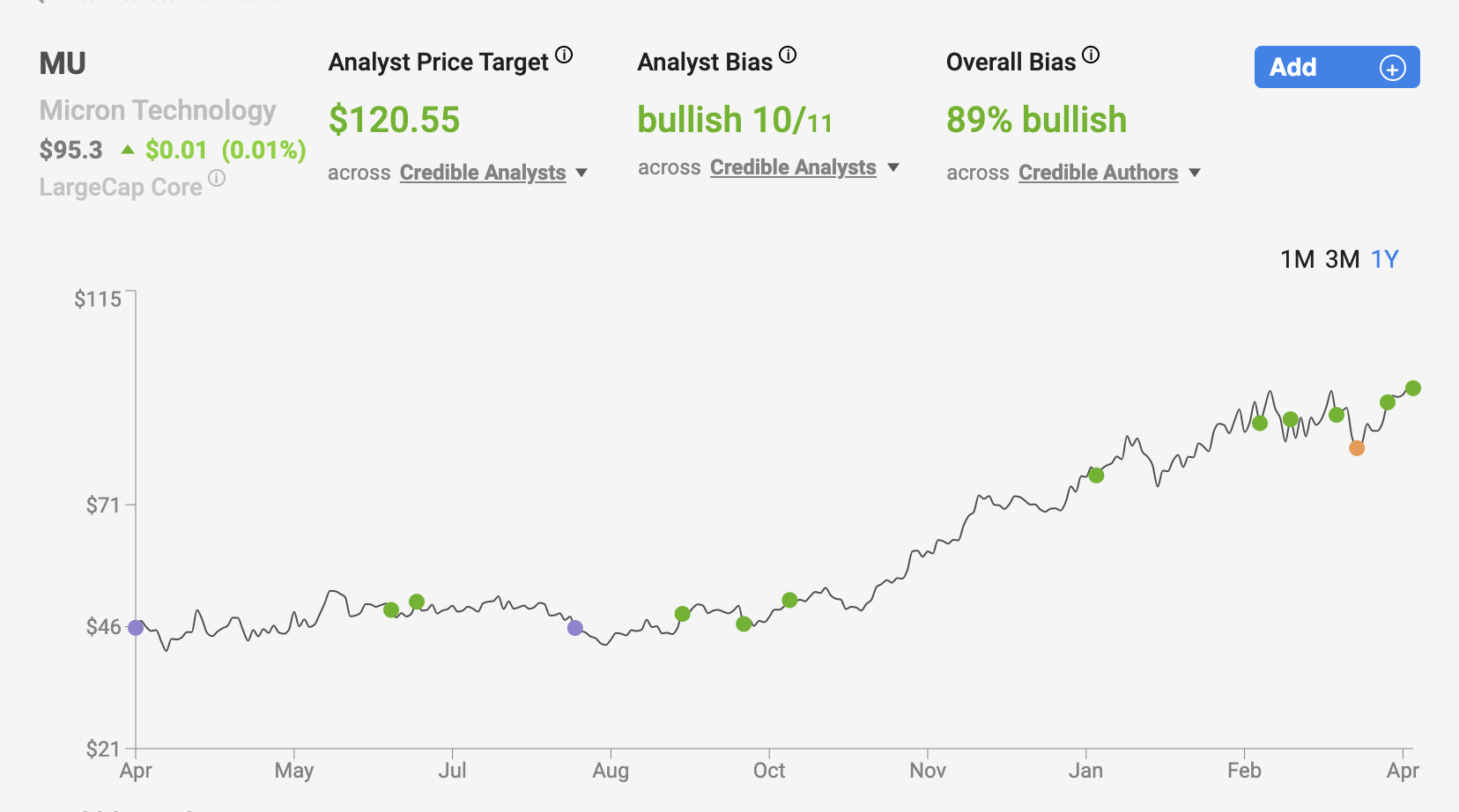

Since the start of 2021, we’ve seen 18 top-rated analysts provide price targets for MU shares. The average price target presented by these 4 and 5-star Nobias analysts is $117.22. Today, MU shares trade for $95.30, which means that the mean Wall Street target calls for 23% upside from here.

Granted, a 23% gain isn’t going to allow most investors to go buy a yacht and retire to tropical waters somewhere; however, when compared to the high single digit average that the broad market has produced over the very long-term, this 20%+ upside potential begins to look quite attractive. If an investor is able to compound his or her wealth at a 23% clip, they will double their wealth every 3.1 years or so. With this in mind, those who’re truly interested in an early retirement may want to take a look at MU shares.

Micron is certainly not a stock for the faint of heart. The stock is highly cyclical and its recent bottom-line results clearly show this. Over the last 10 years, MU’s annual earnings per share growth rate has come in at -91%, -712%, 121%, 1404%, -16%, -98%, 8167%, 141%, -47%, and -55%, respectively. Those are obviously some very volatile swings. They’re caused by common commodity cycles in the semi-conductor space.

Nicholas Rossolillo, a 5-star Nobias analyst who writes for The Motley Fool, recently wrote a piece highlighting past cycles in the semi-space and touching upon the global shortage of chips that we’re seeing play out right now. Regarding MU’s earnings volatility, he said, “Years of booming sales and high prices can be followed by lean periods when demand falls.”

Rossolillo continues, saying, “These cycles are normal for manufacturing, but the downturn was exacerbated by the U.S.-China trade war. Global supply chains had to be rerouted to account for tariffs and embargoes on sales to certain companies. Then COVID-19 struck, temporarily shuttering chip foundries. And chip companies' customers (like automakers, for example) slowed their purchasing of new hardware and worked down existing inventory during 2020 to manage their cash flow.”

Rossolillo says that in recent years, MU has “done a lot of work to tighten up operations and get more efficient, and it's paid off.” He mentions that the company was able to stay profitable during the last cyclical downturn, “granted, just barely.” But, he has high hopes for the short-term, saying that “shares look like a reasonable deal at 25 times trailing 12-month adjusted earnings per share. Bear in mind this current upcycle will eventually moderate and give way to another downcycle, but for now that's not on the horizon. I remain a buyer of Micron right now.”

Harsh Chauhan, a 5-star Nobias analyst who writes also writes for The Motley Fool recently published an article which agrees with Rossolillo’s outlook, noting that pricing trends in the DRAM and NAND markets, both of which Micron operates in, are attractive in the near-term. Chauhan says, “The spot price of dynamic random access memory (DRAM) has shot up close to 60% since the beginning of 2021, hitting the highest levels seen since March 2019. A huge increase in demand from PCs (personal computers), data center servers, smartphones, and an uptick in automobile production has led to tight supply conditions in the memory market, sending prices higher.”

He notes that Trendforce expects to see DRAM prices rise 13-18%, sequentially during Q2, which is well above the 3-8% price increase that we just witnessed during Q1. Chuahan notes that “A similar trend is anticipated in the NAND flash market as well. UBS recently pointed out that the contract price of NAND memory could increase 5% quarter on quarter in the second quarter of 2021, a big improvement over the initial estimate of a 7% decline. The price growth is expected to gather more pace the following period with a sequential increase of 10%, followed by a 2% increase in the final months of the year.”

Regarding those short-term tailwinds, when looking ahead at consensus estimates, it appears that upwards momentum is going to continue, with analysts calling for 93% earnings-per-share growth this year, 88% in 2022, and 10% in 2023.

This earnings growth is why Billy Duberstein, another 5-star Nobias analyst who writes for The Motley Fool, recently said, “Instead of trying to ride short-term momentum, investors are likely much better off investing in strong companies with excellent long-term growth prospects and reasonable prices.” He went on to say that Micron is an attractive company to buy as we move into April, highlighting the company’s recent earnings report, in which “Revenue grew 30% year over year as DRAM pricing rebounded, and adjusted (non-GAAP) earnings per share of $1.13 beat analyst expectations.”

He’s bullish on MU’s short-term prospects, noting that the company provided “Guidance of $1.62 next quarter, or 43% sequential growth, showed continued strength as Micron enters a major DRAM upcycle.” Duberstein says, “what has analysts really excited is that Micron isn't significantly ramping up capital expenditures, even with a current shortage.”

MU has been known to become overzealous with its supply, ultimately resulting in cyclical downturns as boom/bust cycles occur in the semiconductor space. However, even during today’s bottleneck in the chip space, MU appears to be showing discipline on the supply side.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

The increased global demand for semiconductors likely isn’t going to wane anytime soon, and therefore, it’s likely that this commodity cycle is longer lasting than prior events. And, with this in mind, Duberstein concludes, that even after the stock’s nice rally in recent months (MU shares are up 26.76% year-to-date) the company “only trades at 8 times the prior cycle's peak earnings of $11.51 in 2018. If this current upcycle is bigger and better, Micron's stock may just be getting started.” The obvious risk here is that once the cycle ends and Micron’s bottom-line growth stops, it is likely to experience significant negative volatility.

Commodity cycles are largely based on macro economic trends and therefore, they’re very difficult, if not impossible, to accurately predict. For instance, prior to the U.S/China trade war and/or the COVID-19 pandemic, very few analysts or investors could have known how quickly demand trends would change. And, very few (if any) analysts or investors are going to be able to predict the next black swan event that disrupts demand throughout the global supply chain, resulting in yet another commodity cycle coming to an end.

With this in mind, MU is likely a stock that is only going to appeal to investors with strong intestinal fortitude or traders who’re looking to be nimble and play short-term demand trends (which are much easier to predict than long-term cycles). But, as the Wall Street analysts mentioned above, as well as the 5-star contributors cited in this piece note, the short-term sentiment surrounding MU shares is decidedly positive and momentum appears to be headed towards more upside...for those who dare to ride it.

Disclosure: Nicholas Ward has no position in any company mentioned in this article. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.