NextEra Energy: Does Future Growth Justify Today’s High Valuation Premium?

Although the transition away from fossil fuels and towards a green energy future seems undeniable at this point in time, many of the stocks in the renewable energy space, which had experienced a strong rally throughout much of 2021 thus far, have begun to experience a sell-off in recent weeks. It’s unclear what caused this sentiment shift. Valuation is likely at play. No equity ever goes up in a straight line, after all. What’s more, the initial exuberance related to the Biden Administration’s major infrastructure spending plans, which involved heavy investments into renewable energy, is beginning to wane.

In recent weeks, it has become clear that compromise is necessary with Republicans, who appear to be much less interested in a “Green New Deal” type of package, for such a large stimulus deal to pass. Furthermore, Republicans appear to be wary of the overall price tag associated with the proposed infrastructure deal, meaning that any deal that makes it through Congress will likely involve much less stimulus and spending than was originally proposed.

What’s interesting is that while trillions of stimulus spending will obviously be bullish for renewable focused names and utility stocks, the green energy movement benefits from secular tailwinds and therefore, even if the stimulus bill never makes it through the halls of Congress and onto Biden’s desk in the Oval Office to sign, it’s very likely that the positive growth trajectory over the long-term in the renewable space remains intact. And with this in mind, we wanted to highlight the recent share price movement of one of the market leaders in renewable energy production, NextEra Energy (NEE), which has been involved in the recent sell-off.

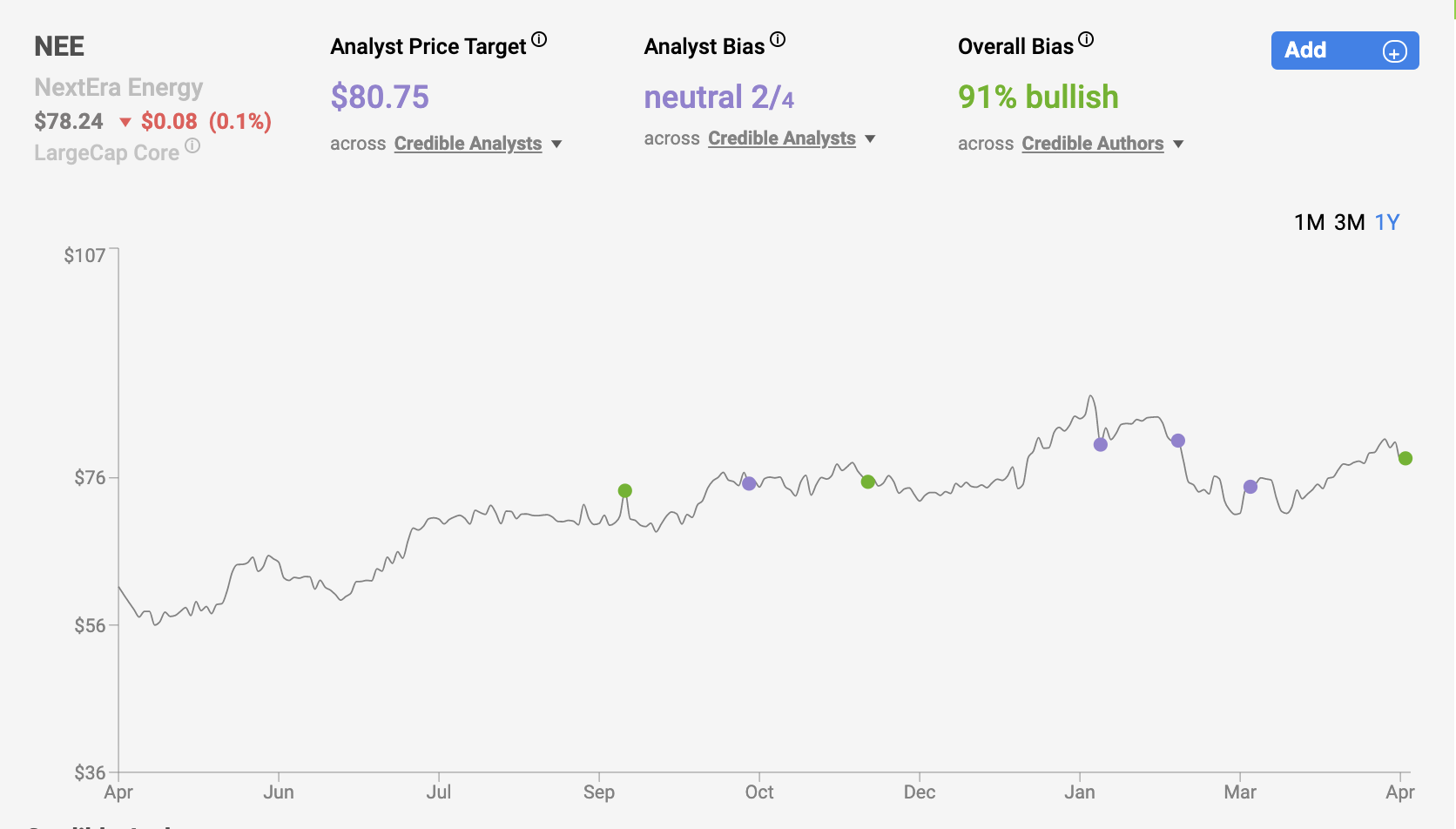

NEE shares are down roughly 3.5% during the past week, pushing their year-to-date returns down to just 1.4%. The S&P 500 is up roughly 11.5% year-to-date thus far, meaning that NEE shares have massively underperformed the broader index. This relative underperformance has led a handful of analysts coming out with bullish opinions in recent weeks.

Right now, when looking at the 4 and 5-star analyst that the Nobias algorithm tracks, we see 6 opinions leaning bullish with just 1 analyst trending bearish with their outlook. With that in mind, it appears that NEE may be an attractive option for investors looking to increase their exposure to renewables. Rekha Khandelwal, a 5-star analyst who writes for The Motley Fool certainly thinks so. She recently penned an article titled, “Is NextEra Energy Stock A Buy?” which offered a strong bullish outlook on the stock. She began her piece by stating that “NextEra Energy has delivered an impressive performance over the years. Its adjusted earnings per share (EPS) grew by 10.5% last year.” This double digit bottom-line growth is rare to find in the utility space, which is generally known for slow and steady revenues and earnings growth. What’s more, Khandelwal notes that NEE’s future growth prospects remain attractive, saying, “The utility expects adjusted EPS to range from $2.40 to $2.54 for 2021, which, at its midpoint, is nearly 7% higher than 2020. Moreover, it expects from 6% to 8% growth in adjusted EPS over the next two years.”

Daniel Foelber, a 4-star analyst who also writes for The Motley Fool, recently wrote an article highlighting his bull case for NextEra, in which he touched upon the company’s operations and stellar past performance. He noted that NEE is best known for its Florida Light and Power Company holdings.

Foelber said, “NextEra's core business is Florida Power & Light (FPL), which is the largest utility in Florida. FPL generates the vast majority of its power from fossil fuels, although it has added renewable capacity, too. FPL's claim to fame is its steady profits and low rates for customers. In a win-win for both NextEra and its customers, FPL's residential customers pay 30% less than the national average.” He continues, mentioning that “NextEra has been using FPL's extra cash and debt to fund its renewable arm, NextEra Energy Resources (NEER).”

Looking at NextEra’s investor relations website, we see that NextEra Energy Resources is “the world's largest generator of renewable energy from the wind and sun and a world leader in battery storage. Through its subsidiaries, NextEra Energy generates clean, emissions-free electricity from seven commercial nuclear power units in Florida, New Hampshire and Wisconsin.”

This combination of reliable earnings from the traditional (and very efficient) utility in Florida and the growth potential of renewables has allowed NEE to post performance well above its peer average over the long-term.

Foelber notes that “Between 2005 and 2020, NextEra grew its adjusted earnings per share (EPS) and dividends per share at compound annual growth rates of 8.7% and 9.6%, respectively.” And circling back to Khandelwal’s piece, we see that the company continues to invest heavily into future growth projects, which create continued strong growth potential moving forward. She said, “NextEra spent $14 billion on capital projects in 2020. The company expects to spend around $44 billion on capital projects through 2025, including nearly $4 billion on wind and solar assets.”

Foelber mentioned the company’s growth plans as well, saying, “To put into perspective the sheer scale of this endeavor, consider that NEER had a renewable capacity of roughly 22 gigawatts (GW) at the end of 2019. After adding 5.8 GW of renewable capacity in 2020, NEER plans on adding an additional 23 GW to 30 GW of capacity by 2024, bringing its total renewable capacity to between 50 GW and 60 GW. Most of NEER's existing and planned renewable capacity is wind energy.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

However, there is downside to all of this growth: valuation. Generally speaking, investors are willing to pay higher premiums for stock with reliable growth prospects. However, high premiums do tend to increase risk and lower future return prospects and at a certain point, the valuation gaps between competitors can become so large that the best-in-breed pick in a given sector/industry no longer looks attractive, on a relative basis. For many, this has been the case with NEE in recent years.

Khandelwal notes, “With a forward price-to-earnings ratio of 29, NextEra Energy looks pricey compared to its top utility peers, which are all trading at forward P/E ratios of around 18.” Not only does this price-to-earnings ratio make NEE look expensive relative to its peers, but this ~29x multiple is always well above the company’s own long-term historical averages. NEE’s 5 and 10-year average blended price-to-earnings ratios are 23.5x and 19.8x, respectively. As you can see, there is a clear premium being placed on shares in the present day. However, Khandelwal justifies this, using forward growth, saying, “if we consider NextEra Energy's expected earnings growth, its valuation looks much better. NextEra's forward price-earnings-to-growth or PEG ratio is 0.4 compared to Southern Company's (SO) ratio of 1.4.”

Frankly put, only time will tell if NEE’s growth prospects come to fruition and eventually justify today’s premium. All equities are risk assets and their prices are generally based upon expectations of future cash flows. Investors betting on NEE at roughly 30x earnings are potentially putting outsized risk onto the table. Yet, Khandelwal appears to be comfortable with the risk/reward proposition that NEE shares offer today, saying, “Simply put, a company growing at a higher rate should trade at a higher P/E than another one that is growing at a lower rate, all other things being equal. Generally, a ratio below one indicates that a stock isn't overpriced, based on its expected growth.” And, she concluded her piece with clearly bullish commentary, saying, “NextEra Energy's steady operations combined with its huge renewables portfolio makes it an attractive buy. Its growth plans and outlook inspire confidence in its ability to continue generating peer-leading dividend growth. The stock's recent pullback offers an entry point to build your position for the long term in this top utility.”

Disclosure: Nicholas Ward has no positions in any equity mentioned in this article. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.