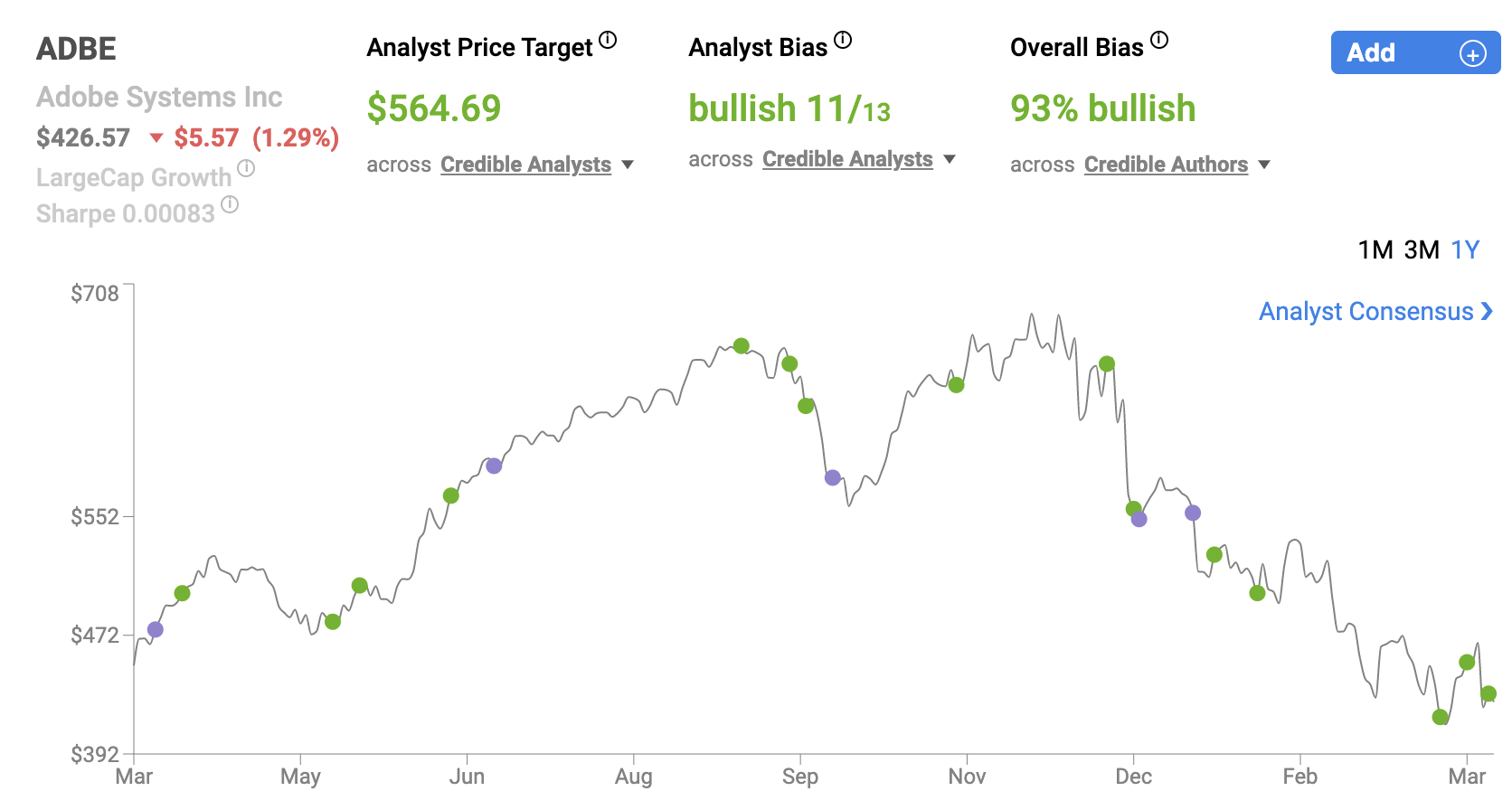

ADBE with Nobias Technology: Adobe shares drop nearly 39.5% from their 52-week highs

For years, Adobe was one of the hottest stocks on Wall Street. During the last 10 years, ADBE shares are up 1,121.20%. And, if it wasn’t for the stock’s recent precipitous declines, these trailing results would look immensely stronger.

Adobe’s 52-week high is $699.54, set in late 2021. Today, shares trade for $422.90, down approximately 39.5% from those highs. ADBE shares are down 25.07% on a year-to-date basis. And, just yesterday, the stock fell 9.34% (throughout much of the trading session, shares were down 10%+) on disappointing first quarter results.

There is little doubt that this former market darling has lost a lot of its luster. However, the stock continues to post strong operational growth. And, when looking at the analysis performed by the credible authors and Wall Street analysts that the Nobias algorithm tracks, it appears that the stock’s recent sell-off has been overdone.

Although the stock has suffered throughout 2022, Adobe’s results last year still represented a strong growth trajectory. Julian Lin, a Nobias 4-star rated author, recently published a bullish article on ADBE shares which highlights its fiscal 2021 results.

ADBE March 2022

Lin said, “ADBE closed out its FY21 with strong results. It beat on all of its original targets, delivering $15.8 billion in revenue and $12.48 in non-GAAP earnings per share.” He continued, “Those results reflected 22.7% and 23.6% growth, respectively. The strong results were fueled in large part due to the 29% revenue growth at its Document Cloud division, powered by its move into the e-signature market. ADBE also generated robust growth at Creative Cloud (includes the Photoshop software) and Experience Cloud (online marketing and web analytics products).”

Lin touched upon Adobe’s balance sheet saying, “ADBE maintains a strong balance sheet with $1.7 billion in net cash. The $4.1 billion in debt suggests that ADBE management is willing to eventually lever up the company to boost shareholder returns.” And, he highlighted the company’s year-end fiscal 2022 guidance saying, “ADBE has guided for the next fiscal year to see revenue grow 13.3% and for earnings per share to grow 9.8%.”

Lin noted that in a pessimistic scenario, the stock could generate annual returns of 13%-15% moving forward (based upon earnings growth projections). He concluded his report saying, “I rate shares a buy as part of a lower-risk tech allocation, as the share repurchase program may help the stock be among the earliest to rally in any tech recovery.”

Lin isn’t the only credible author that we track who has recently published a bullish report on ADBE shares. Nobias 5-star rated author, Daniel Foelber, recently wrote an article titled, “1 Growth Stock, 1 Value Stock, and 1 Cryptocurrency to Buy for 2022” and Adobe was the growth stock that he put a spotlight on. Foelber said, “The best growth stocks aren't the fastest growers, but, rather, are the companies that have industry-leading positions in exciting marketplaces, offer strong profit, and generate consistent positive free cash flow. If the last few years have taught us anything, it's that the market favors this balanced level of growth at a reasonable price over growth at all costs. And few companies do it better than Adobe.” He continued, “A few decades ago, discussions of recession resilience were usually reserved for consumer staple companies like Procter & Gamble that make products people need no matter how the economy is doing. Today, one could argue that companies like Adobe are digital staples, or enterprise staples because their solutions are needed to conduct business. Given its massive moat, improved profitability, and the fact that it's down 26% from its 52-week high, Adobe stands out as a solid all-around growth stock to buy in 2022 and hold forever.”

Obviously Adobe’s sell-off has accelerated since Foelber published that piece, with shares currently down roughly 40% from 52-week highs. And yet, looking at the company’s recent quarterly results (which sparked yesterday’s 10% sell-off), it’s clear that this company remains on a very reliable growth runway.

When Adobe reported its first quarter earnings, the company beat Wall Street consensus estimates on both the top and bottom lines. ABDE’s Q1 revenue totaled $4.26 billion, which was $20 million above expectations and represented 9.0% year-over-year growth. On an adjusted basis, this $4.26 billion revenue figure represented 17% year-over-year growth. ADBE’s Q2 non-GAAP earnings-per-share came in at $3.37, beating Wall Street’s estimate by $0.03/share.

During the company’s first quarter report, Adobe’s CEO, Shantanu Narayen, was quoted saying, “Adobe achieved record Q1 revenue as Creative Cloud, Document Cloud and Experience Cloud continue to be pivotal in driving the digital economy. Adobe is committed to empowering individuals, transforming businesses and connecting communities.”

The company’s CFO, Dan Durn, said, “Adobe’s Q1 results reflect the company’s strong execution and resilience through unprecedented circumstances. Our momentum, product innovation and immense market opportunity position us for success in 2022 and beyond.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Adobe’s Q1 report shows that each of the company’s primary operating segments posted double digit y/y growth on an adjusted basis. The company said: “Digital Media segment revenue was $3.11 billion, which represents 9 percent year-over-year growth or 17 percent adjusted year-over-year growth1. Creative revenue grew to $2.55 billion, representing 7 percent year-over-year growth or 16 percent adjusted year-over-year growth1. Document Cloud revenue was $562 million, representing 17 percent year-over-year growth or 26 percent adjusted year-over-year growth1.”

During Q1, Adobe’s cash flows from operations totaled $1.8 billion. The company took advantage of recent share price weakness, using its cash flows, as well as the cash on its balance sheet, to repurchase approximately 3.8 million shares, worth $2.1 billion, showing that ADBE management and its Board of Directors appear to believe that shares are cheap at current valuations. It appears that this level of growth disappointed Wall Street (otherwise, we wouldn’t have seen such a drastic sell-off after the Q1 results were posted); however, when looking at the sentiment expressed by the credible authors and analysts that we track with the Nobias algorithm, there is a very strong bullish bias surrounding shares.

93% of the opinions recently expressed by credible (4 and 5-star rated) authors have been “Bullish”. And, when looking at the credible Wall Street analysts that our algorithm tracks (once again, only those with 4 and 5-star Nobias ratings) we see that the average price target being applied to ADBE shares is currently $581.09. After ADBE’s nearly 10% sell-off its shares are trading for $422.90. Relative to that $581.09 price target, today’s share price represents upside potential of approximately 37.4%.

Disclosure: Nicholas Ward is long ADBE. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.