COIN with Nobias Technology: Case Study on Coinbase

Coinbase (COIN) was one of the hottest new stocks to begin public trading in 2021. The stock came public via a direct listing in April of 2021. At the time, market markers expected the stock to open trading in the $250 range; however, COIN shares opened trading in the $381 area. They quickly rose to $429.54 before trading down to $328.28, where they closed after their first day trading on the Nasdaq.

This move equated to an $85.8 billion market cap on a fully diluted basis. With the benefit of hindsight, the violent trading that COIN shares experienced on their first day of trading was a precursor of things to come. Since April of 2021, COIN shares have sold off down to the $220 area, risen back up to the $368 range, and then most recently plunged down to all-time lows of $40.88.

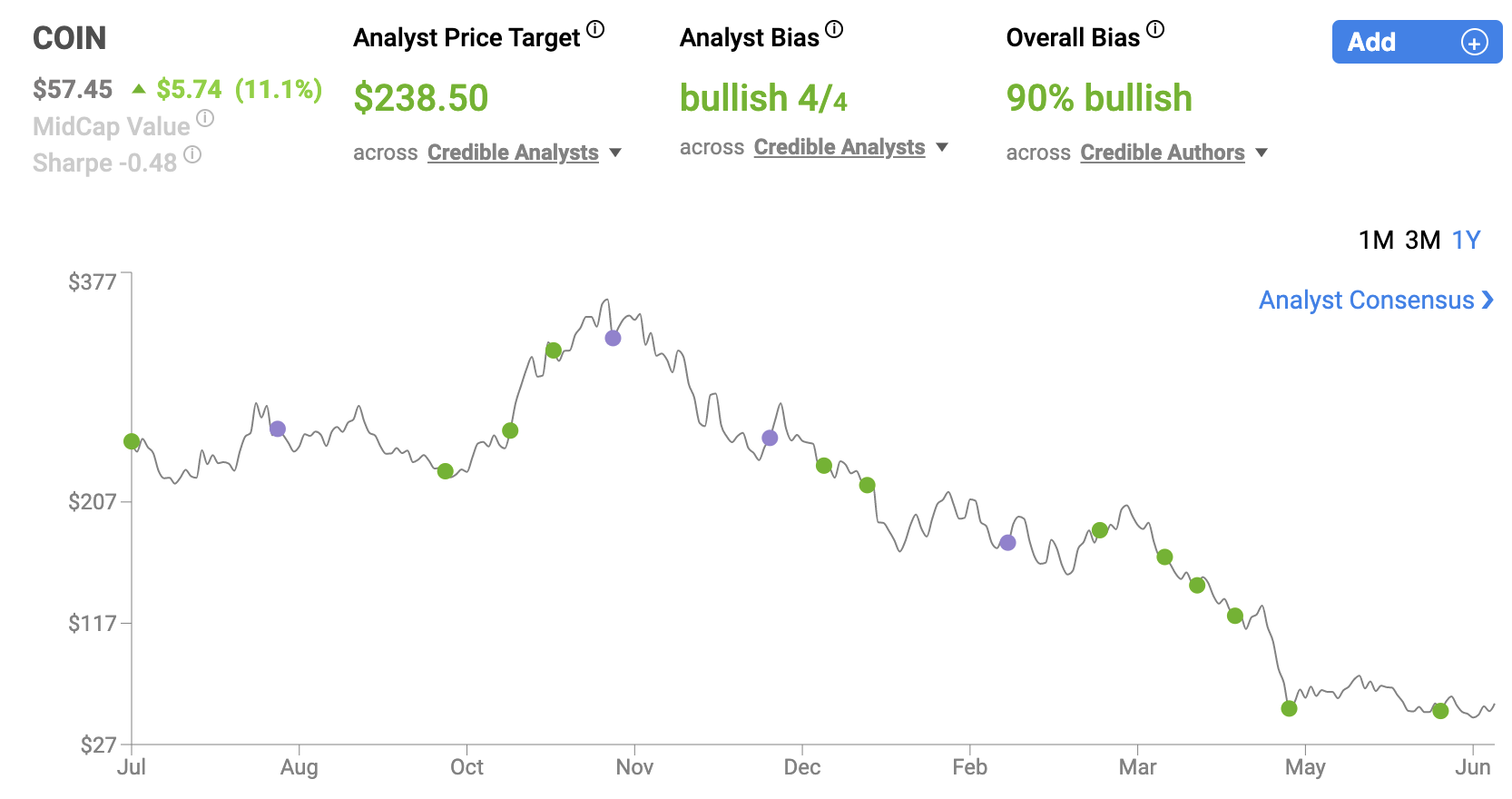

Today, Coinbase shares trade for $49.04, down roughly 86.7% from their 52-week highs. And, while there is no sign that volatility is about to abandon these shares, the credible authors and analysts that we track with the Nobias algorithm remain overwhelmingly bullish on COIN shares.

COIN Jun 2022

Coinbase posted first quarter earnings on May 10th, missing Wall Street consensus estimates on both the top and bottom lines. Since then, COIN shares have fallen by approximately 32.8%. Nobias 4-star rated author, David Trainer, covered Coinbase’s Q1 report in a recent article published at Seeking Alpha titled, “Q1 2022 Earnings Shows Coinbase's Struggles”.

Trainer said, “Coinbase's 1Q22 results and guidance do not bode well for the future, and we think shares are worth as little as $17/share even with optimistic assumptions for long-term margins and revenue growth.”

Regarding the company’s fundamentals, Trainer wrote: “As noted in our prior update in March 2022, the growth and profitability achieved by Coinbase in 2021 was unsustainable - 1Q22 proved as much. In the quarter Coinbase's:

net operating profit after-tax (NOPAT) margin fell to -19%, down from 43% in 1Q21

invested capital turns fell from to 0.4, down from 1.4 in 1Q21

return on invested capital (ROIC) fell to -7%, down from 58% in 1Q21

free cash flow (FCF) was -$1.4 billion, compared to $969 million in FCF in 2021.”

Looking at the guidance that COIN management provided, Trainer stated, “Going forward, we expect Coinbase's margins and revenue growth rates to decline as competition increasingly eats into its business. Increased volatility, or further downward movement, in the crypto market could also spook retail investors after big losses so far this year.”

Regarding that guidance, he noted: “Guidance shows:

MTUs [monthly transacting users] is expected to be lower in 2Q22 than 1Q22

total trading volume expected to be lower in 2Q22 than 1Q22

expected range for MTUs in 2022 anywhere from 5 to 15 million, not exactly a precise estimate

ATRPU in 2022 is expected to return to "pre-2021" levels, which certainly implies a decline”

Trainer also noted a quote that appeared in the 10Q that Coinbase filed with the SEC and the potential for it to further damage investor sentiment.

COIN stated, "in the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors." Trainer continued, “This public acknowledgement could spark fear in the company's clients. The fear of bankruptcy proceedings could drive clients to cash out their investments as quickly as possible, further weakening Coinbase's business, and bringing the company even closer to bankruptcy.”

Trainer concluded, “Looking forward, we expect the company's profitability to diminish as expenses rise and growth slows with crypto adoption losing momentum and regulations rising.”

However, shortly after COIN’s earnings, Nobias 4-star rated author, Investor Trip, posted a bullish piece on COIN, titled, “Coinbase: Be Greedy During The Crypto Market Crash”. Investor Trip acknowledged COIN’s recent poor performance, stating, “The company posted an awful Q1 2022 due to the crypto bear market and investors started fleeing for the exits. COIN stock is down 78% YTD due to the current crypto bear market.”

Yet, they continued, “However, I've been a passionate user of Coinbase since 2018 and won't sell a single share during this current market crash.” Regarding the Q1 miss, Investor Trip said, “Coinbase suffered a big dip in monthly transacting users, trading value, and assets on the platform in comparison to Q4 2021, triggering a massive 25% selloff after Q1 2022 earnings release.”

The author suggested that the numbers weren’t as bad as they appeared, though, writing, “Lower crypto prices caused a $258 million impairment charge because the SEC requires all companies holding crypto assets to include any losses when they fall below their cost basis. Removing impairment charges, Coinbase lost around $172 million per quarter.”

Furthermore, Investor Trip seems to suggest that COIN’s near-term future may not be as bright as their bullish title suggests, saying, “Bitcoin prices have fallen substantially since the beginning of 2021, which has caused COIN shares to fall. This is completely normal as Bitcoin enters the 2nd half of its current halving cycle. In fact, Bitcoin has historically fallen as much as 80% during the bottom of its bearish cycle. That means COIN stock could trade much lower as we head towards the 2nd half of 2022.”

Long-term, the author believes that COIN’s steps with regard to revenue stream diversification are what sets the stock up to outperform. Investor Trip said, “Coinbase turned 10 years old this year and is no longer just a cryptocurrency broker and exchange.” They continued, “In April, Coinbase launched its NFT marketplace to compete with Opensea and generate revenue from the growing NFT industry but initial activity has been slow.”

“Secondly,” they wrote, “5.8 million Coinbase users staked their crypto on Coinbase to generate yield with their assets in Q1 2022.” “Thirdly,” Investor Trip said, “Coinbase plans to launch crypto derivatives products similar to options trading that allow users to profit from short and long-term crypto price movements. In February, Coinbase acquired FairX to help ease its transition into derivatives.”

Finally, Investor Trip concluded that COIN is “all about user growth” stating, “Coinbase user growth grew at a 75% CAGR over the last year as the company continues to rack up more user growth despite falling crypto prices.” Therefore, Investor Trip wrote, “Long-term investors have a wonderful opportunity to acquire an industry-leading company with a growing user base at rock bottom prices.”

Regarding the fearful statement that COIN made about the potential of bankruptcy, Investor Trip said, “Also, Coinbase filed a shelf registration with the SEC and may need to sell stock in order to stay afloat. Coinbase CEO Brian Armstrong denied that the company is at risk of bankruptcy on Twitter so hopefully the company has plenty of cash to make it through the crypto bear market.”

In a recent series of tweets, Armstrong said, “Your funds are safe at Coinbase, just as they’ve always been.” Investor Trip also noted, “Many investors have expressed concerns about Coinbase filing for bankruptcy due to running out of cash. The company held $6.1 billion in cash on its balance sheet at the end of Q1 (including $180 million in USC and $1 billion in various crypto assets).”

Ultimately, the author concluded, “Cryptocurrency is the future of finance and isn't going anywhere. I expect Coinbase to remain a leader in the industry for years to come.” While COIN shares have continued to trend lower post-earnings, Shrey Dua, a Nobias 4-star rated author, noted that famed growth investor, Cathie Wood of ARK Investments, continues to buy COIN shares.

On June 3rd, Dua wrote, “It seems crypto exchange Coinbase is Cathie Wood’s latest obsession. Wood has continued to buy COIN stock despite its recent tumble. Indeed, Wood, known for her high-growth strategy, has apparently pegged Coinbase as the latest undervalued disruptor.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Dua continued, “Wood has made 20 purchases of COIN since March 25, buying between 3,900 and 187,000 shares with each investment. In fact, in the past week alone, Wood has purchased COIN on three separate occasions across her various funds.”

It’s important to note that Wood’s funds have experienced a lot of negative volatility during 2o22, which has caused certain investors to question her acumen (ARK’s leading fund, the ARK Innovation ETF (ARKK) is down 57.50% on a year-to-date basis. However, many growth stock effecianados still look to Wood for inspiration so her bullish outlook on COIN shares is certainly an anchor for bullish investors to hold on to during the stock’s recent volatility.

With such strong opinions, on either side of the bull/bear argument, to be found related to COIN, it’s important to look at the consensus of the communities of credible authors and analysts that the Nobias algorithm tracks.

Regarding credible authors (only those with Nobias 4 and 5-star ratings), 90% of recent reports focused on Coinbase have included a “Bullish” bias. And, the average price target currently being applied to COIN shares by the credible Wall Street analysts that we track (once again, only those with 4 and 5-star Nobias ratings) is $238.50. Relative to COIN’s current share price of $49.04, this consensus price target represents upside potential of approximately 386%.

Disclosure: Nicholas Ward has no COIN position. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.