Ford: Lack of consensus on the future

Ford stock does appear to be very cheap, based upon its 2021 EPS expectations; however, if Ford cannot carve out meaningful market share in the EV space, this growth is unlikely to sustain itself. Due to the fact that stocks are evaluated on their future cash flow potentials and the inherent uncertainty attached to Ford’s ability to capture meaningful market share in the EV market right now, this remains a battleground stock.

Throughout 2021, one of the most popular ideas in the disruptive, growth oriented area of the stock market is electronic vehicles. From mega-cap names like Tesla (TSLA), unproven start-ups in the SPAC space, to the traditional automotive companies who’re attempting to transition from lineups centered around combustible engines into EV’s as the world marches on into the 21st century, which is expected to be known for the transition to green energy and autonomy, investors are placing bets.

At this point in time, it’s too early to crown the eventual winners and losers. Only time will tell who eventually perfects the technology which results in large market share of this burgeoning industry. However, as Will Ebiefung of the Motely Fool put it in a recent article, “Everybody wants a good deal, and there are different ways to find one in the stock market. Some investors play it safe by buying blue-chip companies with consistent profits, while others take a riskier approach by betting on comeback stories like Ford Motor (F).”

Ebiefung cites data from consulting firm, Deloitte, which states that by 2030, 32% of all new cars sold with be EV’s. This represents an annual growth rate of 29% throughout the present decade. With this sort of growth in mind, there’s no wonder that companies, new and old, are fighting hard for a slice of this growing pie. Ebiefung’s piece makes it clear that Ford has big plans for its EV future, noting that the company’s CEO, Jim Farley, recently said, "We are not going to cede the future to anyone when it comes to electric vehicles." Ebiefung discussed Ford’s plan to invest $29 billion into EV/autonomous technologies by 2025, with a focus on the areas of the auto space where it already holds strong market share positions, such as pick up trucks, transit vans, and sports cars.

IAM News, recently reported that “Ford's all-electric Mustang Mach-E is starting to arrive in dealerships, which will be followed by the firm's first E-Transit commercial van later in the year. The beloved all-electric F-150 pickup is scheduled for release in the mid-2020s.” The IAM News piece also highlighted Ford’s recent plans “to phase out gas cars in Europe by 2030” further emphasizing its commitment towards EV development, worldwide.

And yet, the market doesn’t appear to be rewarding Ford, when it comes to a growth premium associated with its EV potential (at least, on a relative basis to its pure-play peers in the EV space). When it comes to valuation, Ebiefung says, “Tesla boasts a forward price-to-earnings (P/E) ratio of 200 and a market cap of $752 billion. Upstart EV maker NIO (NIO), which isn't profitable on an annual basis, trades for 32 times sales with a market cap of $89 billion -- almost twice the size of Ford.” Ford, on the other hand, which has experienced a nice rally as of late, with shares rising by more than 52%, year-to-date, currently trades with a forward price-to-earnings multiple of just 11.8x.

Ford’s current market cap is $53.2 billion, which is respectable, but still pales in comparison to Tesla’s, even though Ford’s annual cash flows dwarf’s Tesla’s. In 2020, Ford generated $18.5 billion in free cash flow, compared to Tesla’s annual FCF of $2.78 billion. Ebiefung concluded his bullish article, writing, “Ford stock is dirt cheap compared to much-hyped electric vehicle rivals like Tesla and NIO, making the company a good bet for investors who want to get in on the ground floor of this rapidly expanding opportunity.”

John Roevear, also of The Motley Fool, recently echoed Ebiefung’s bullish sentiment, highlighting his belief that Ford is a strong re-opening play as the vaccine rollout continues. Roevear said, “Auto sales tend to rise early in most economic recoveries, for a simple reason: People and businesses tend to postpone vehicle purchases when times are tough. And when that happens, the automakers with the freshest products tend to see the biggest bounce in both sales and profits. The post-COVID recovery won't be quite the same as a post-recession economic recovery, but I think there will be some parallels -- and I think it's enough of a parallel to warrant a closer look at Ford right now.”

Overall, analysts agree with this thesis. Right now, the consensus EPS growth rate attached to Ford in 2021 is 176%. What’s more, the consensus growth estimate for 2022 is 34%. However, even with such strong growth expectations in the future, it’s important to note that Ford’s 2022 EPS expectation of $1.51/share is still far below the $1.71/share that the company generated in 2017, showing the operational malaise that Ford has experienced in recent years as sales and cash flows struggled.

Now, on the flip side of this bounce back coin, it’s important to note that this economic sensitivity and the bottom-line volatile that it creates can be enough to keep conservative investors out of Ford shares. For instance, during 2020 and the COVID-19 pandemic, Ford’s earnings-per-share fell by 66%. And, this negative result came on the heels of a -8% EPS growth rate in 2019 and a -27% EPS growth rate in 2018.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Looking backwards, we see that Ford has posted positive earnings-per-share growth in just 3 out of the last 10 years. This points towards more secular growth issues, regarding the company’s product line. Management has taken steps to address this in recent years by cutting unprofitable lines and focusing on vehicles, such as the f-series pickups, that really resonate with consumers. However, the fact is, with the stock rising so far so fast, many of the analysts that we track offer a cautious outlook on shares.

Ford stock does appear to be very cheap, based upon its 2021 EPS expectations; however, if Ford cannot carve out meaningful market share in the EV space, this growth is unlikely to sustain itself. Due to the fact that stocks are evaluated on their future cash flow potentials and the inherent uncertainty attached to Ford’s ability to capture meaningful market share in the EV market right now, this remains a battleground stock.

Right now, Nobias tracks fourteen 4 and 5-star analysts who offer buy/sell opinions on Ford. Today, 9 of the opinions are bullish; however, 5 analysts have sell ratings on the stock, pointing towards a general lack of consensus.

Disclosure: Nicholas Ward does not have a position in Ford. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Facebook: Are publication and privacy issues over?

As we continue to forge into the digital age, there is no doubt that ongoing internet regulation is necessary. Facebook says as much, highlighting the fact that it is on board with an up-to-date set of rules for digital media platforms. There is no telling how quickly major reform like this will pass in the U.S. and abroad; yet, the Australian narrative points towards there being significant growing pains along the way.

For years, the classic “F.A.A.N.G.” stocks have been market leaders, not only is the tech-heavy NASDAQ, but in the broader S&P 500 index as well. F.A.A.N.G. stands for Facebook (FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and Google (GOOGL) (which has been re-named, Alphabet, since this acronym was coined). Investors who’ve owned any of these stocks over the years have done quite well for themselves, with each and every one of the big-tech players producing significant alpha.

However, even the best of the best tech names got caught up in the recent NASDAQ 100 sell-off. Although we’ve witnessed a large rally thus far this year, when looking at the returns that these famous F.A.N.G. names have produced during the last month, we see that all 4 stocks have generated negative total returns. Facebook shares are down 2.56% during the last month. Amazon shares are down 6.97% during the same period. Netflix shares are down 10.48% during the prior month. And, Alphabet shares are down 2.41%.

When looking at the valuations that these stocks present, Facebook is the cheapest, by a fairly significant margin, when talking about a blended price-to-earnings ratio, as well as a forward looking P/E ratio. At Facebook’s current share price of $273.88, shares are trading with a 26.4x blended P/E ratio and a forward P/E ratio of 23.75x attached to them.

Facebook grew its bottom-line by 57% in 2020 and right now the consensus analyst estimates for 2021, 2022, and 2023 earnings-per-share growth are 14%, 16%, and 18%, respectively. It’s rare to see a mega-cap stock like Facebook (Facebook’s current market cap is $754 billion) produce such strong and reliable double digit bottom-line growth. And, in today’s relatively expensive market (the forward P/E ratio attached to the S&P 500 is currently 21.9x, which is well above its 5 and 10-year average P/E ratios of 17.7x and 15.8x, respectively) it’s even more rare to find relatively low PEG ratios attached to blue chip stocks.

When analysts look at Facebook’s 23.7x forward P/E ratio and compare it to the 15%+ consensus long-term growth rate, they put the stock into the “growth at a reasonable price” or “GARP” category. In her recent Gurufocus article, Sydnee Gatewood reported that investment management firm, Ruane Cunniff, had this to say about Facebook’s valuation when discussing their Q4 review of the company: “We believe this risk is reflected in the shares with Facebook trading for ~24x consensus forward earnings, a near market multiple for a dominant social media enterprise whose earnings we expect to grow far in excess of the overall economy for years to come.”

However, it hasn’t just been valuation on the minds of analysts. In the Ruane Cunniff report, the advisers said, “Not surprisingly, in a year that saw parts of the globe locked down for extended periods, engagement with the Facebook family of apps strengthened.” Regarding Facebook’s app strength and the company’s ability to compete, adapt, and evolve during volatile times in the markets, Anusuya Lahiri, a Bezinga staff writer with a 5-star rating by Nobias’s algorithm recently highlighted some of the company’s recent innovations as Facebook continues to hunt global market share.

She began with news that Facebook recently developed and launched its Instagram Lite product saying, “The app requires just 2MB compared to Instagram’s 30MB. It is compatible with 2G networks, permitting customers in India, Africa, Asia, and Latin America with older internet infrastructure to access the service.”

Instagram Lite still offers the app’s core processes, without TV banner ads and the sharing of video clips. Video ads are largely viewed as some of the most attractive, garnering the highest margins for digital ad platforms like Facebooks; however, this is a case of the company chasing previously unavailable market share, rather than prioritizing ARPU (average revenue per user).

Historically, Facebook’s ARPU figures have been quite low historically (especially relative to its U.S. and European numbers), so the launch of Instagram Lite isn’t likely to negative impact the company’s margins moving forward. Lahiri also highlighted other innovations targeting emerging markets, saying, “Additionally, Facebook in Tel Aviv also developed the Express WiFi service to extend internet access to around 20 countries in Africa, Asia, and South America.”

However, even with such strong growth in mind, the Ruane Cunniff report went on to note that, “While Facebook turned in strong financial performance in a difficult environment, 2020 was not without turmoil as political discourse raged on the company's apps.”

Facebook’s size and scale have attracted quite a bit of negative attention throughout the recent U.S. election season. And what’s more, the company’s privacy policy issues and ongoing disputes regarding internet legislation have put Facebook squarely in the crosshairs of regulators in the U.S. and abroad.

Several of Facebook’s frequent mentions by 4 and 5-star analysts and contributors tracked by the Nobias system focused on the company’s recent “aggressive content blackout” in Australia in response to changes that the country made to its digital content laws, which would have required Facebook to pay news publishers when their content was broadcasted on the Facebook platform.

In the days since the original blackout, Facebook has re-established media coverage in Australia. Motley Fool contributor, Anders Bylund, has covered the ongoing issue recently and said, “The local news sites that were disabled last week are back online as lawmakers agreed to make some changes to the proposed News Media Bargaining Code.”

Bylund continued, noting that the issue between the Australian code and Facebook came down to the fact that “As written, the law requires payments to news media outlets before a handpicked group of online services including Facebook and Google would be able to publish links to their news articles.” However, he said that Australia's code “is getting some tweaks to address Facebook's core concerns” which is what inspired Facebook to go back online in the country.

Facebook put out a statement, in which the company’s Vice President of Global News Partnerships, Campbell Brown, said, "Going forward, the government has clarified we will retain the ability to decide if news appears on Facebook so that we won't automatically be subject to a forced negotiation."

Giulia Bottaro of Proactive Investors reported that in the hours after its ban-reversal, “Facebook has signed a partnership with Australia’s largest media company.” Bottaro said, “The social media giant will host news provided by Seven West Media, which owns the prominent Seven Network, The West Australian, The Sunday Times and Seven Studios among others.” She also reported that Seven West Media recently signed a deal with Alphabet, as well.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

While it’s good news that Facebook and Australia were able to come to an agreement, it’s clear that ongoing publication and privacy issues are far from over for Facebook.

The company recently released a television commercial which highlighted all of the incredible changes that have occured with the internet since its launch, while noting that internet regulations in the U.S. have not changed during the last 25 years since the Telecommunications Act was originally passed in February of 1996.

As we continue to forge into the digital age, there is no doubt that ongoing internet regulation is necessary. Facebook says as much, highlighting the fact that it is on board with an up-to-date set of rules for digital media platforms. There is no telling how quickly major reform like this will pass in the U.S. and abroad; yet, the Australian narrative points towards there being significant growing pains along the way.

Generally speaking, the stock market hates uncertainty. And, with a myriad of potential outcomes at play with regard to regulating digital media platforms, Facebook’s relative discount to its F.A.A.N.G. makes sense. Until these issues are resolved, it appears likely that broad investor sentiment surrounding Facebook will be tepid, at best.

These uncertainties make themselves clear when tracking the 4 and 5-star Nobias analysts as well. Out of the 24 opinions that we track, we see 10 buy ratings, 2 neutral ratings, and 12 sell ratings, showing that Facebook remains a battleground stock.

Disclosure: Nicholas Ward is long AMZN, FB, and GOOGL. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Boeing: Things appear to be looking up

….things do appear to be looking up for Boeing, according to the 5-star analysts that the Nobias algorithm tracks. Last week, Lou Whitman of The Motley Fool, highlighted a recent deal between the U.S. and European regulators to pause aerospace tariffs as a bullish catalyst for Boeing, and its counterpart in the aforementioned duopoly, AirBus, which is domiciled in France.

The travel and leisure industry has experienced profound weakness due to the COVID-19 pandemic. This weakness is ongoing; however, in recent quarters, management teams from companies in this space have begun to provide more upbeat guidance associated with the vaccination roll-out and the thought that herd immunity in many developed nations is a realistic short-term expectation.

Boeing (BA), which is arguably the most iconic company in the travel space, due to its position as a part of the global duopoly in the commercial aerospace market, saw its operational results and its stock price, fall precipitously during the pandemic period. However, in recent months we’ve seen a strong uptick in bullish sentiment surrounding this stock. And, in recent days, Boeing has been tagged as one of the most talked about stocks, by investors, analysts, and bloggers that our algorithm tracks, which inspired us to put together this piece.

Roughly 2 years ago, in early March of 2019, Boeing shares hit an all-time high closing price of $440.62. During the depths of the COVID-19 recession, on March 18th, 2020, BA shares hit their current 52-week low of just $89.00/share, representing a drop of nearly 80%. Since then, we’ve seen BA shares bounce back to the

During the 2014-2018 5-year span, Boeing’s free cash flows increased from $9.08 billion to $23.33 billion. And, coming into 2019, analysts had bullish expectations of continued bottom-line growth. However, unexpected disaster struck.

In late 2018 the world received news of the Lion Air Flight 610 crash. This plane was a Boeing 737 Max. And then, on March 10th, 2019, news broke that Ethiopian Airlines Flight 302 crashed as well. Once again, this was a Boeing 737 Max airplane.

These two crashes resulted in the worldwide grounding of the 737 Max airliner, which was a devastating blow to Boeing’s operations. The 737 Max was meant to be Boeing’s growth catalyst in the fast growing narrow body plane segment. The Max grounding alone would have caused Boeing’s cash flows to crater; however, when the COVID-19 pandemic struck in early 2020, putting further pressure on the aerospace industry at large and therefore, Boeing’s ancillary revenue streams.

Boeing, which was viewed as a free cash flow machine by many investors, saw that metric fall from $23.3 billion in 2018 to -$7.79b in 2019. In 2020, during COVID-19, BA’s free cash flow fell even further, to -$34.64 billion. These negative earnings forced Boeing management to cut its dividend, stop buying back shares, lay off 10’s of thousands of workers, give more than 80,000 employees stock bonuses instead of their annual raises, contribute stock to the company’s pension plan, rather than cash, and raise massive amounts of debt to cover its expenses.

Boeing’s long-term debt was $60.99 billion at the end of 2020. This figure was up drastically from the $8.5 billion in long-term debt that this company had on its balance sheet at the end of 2018.

But, things do appear to be looking up for Boeing, according to the 5-star analysts that the Nobias algorithm tracks. Last week, Lou Whitman of The Motley Fool, highlighted a recent deal between the U.S. and European regulators to pause aerospace tariffs as a bullish catalyst for Boeing, and its counterpart in the aforementioned duopoly, AirBus, which is domiciled in France.

Whitman notes that the European Commission President, Ursula von der Leyen, released a statement after a conversation with U.S. President, Joe Biden, saying, "This is excellent news for businesses and industries on both sides of the Atlantic, and a very positive signal for our economic cooperation in the years to come."

A resolution of this trans-Atlantic trade dispute, which was yet another headwind that Boeing was dealing with, has the potential to be a significant boon for BA’s bottom-line over the long-term, assuming a final deal between the Biden administration and EU regulators comes to pass.

Boeing recently received good short-term news as well. In a separate article posted in early March, Whitman reported that United Airlines added 25 737 Max jets to its recent order and decided to accelerate the delivery of 45 of the 188 737 Max planes that it has on order to the 2022/2023 timeline.

Boeing recently reported February 2021 aircraft sales, which saw 82 sales and 51 cancelations. This marks the first month since November of 2019 that BA’s sales outnumbered cancelations. This news, alongside the recent United Airlines deal, points towards what could be a positive shift in Boeing’s sales data.

Whitman expressed cautious optimism about this news, saying, “Still, investors should note that this news is one small step in a long recovery for Boeing. Until the pandemic is behind us and airlines are able to rebuild their balance sheets, we are unlikely to see the sort of upcycle in new plane orders that Boeing was enjoying before.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Members of the analyst community appear to have more conviction about their bullish outlooks. Morgan Stanley’s Kristine Liwag recently raised her price target on the stock from $230 to $250/share. This raise came after Liwag’s late January upgrade of Boeing, from underweight to overweight, when she said her price target from $165 to $230, saying that Boeing is “a COVID-19 recovery play with upside.”

The early March increase to $250 further solidifies that bullish opinion. This isn’t the only recent upgrade that Boeing has received. Canaccord Genuity’s Ken Herbert recently raised his price target on Boeing from $200 to $275. During his report, Herbert said, “"We are upgrading the shares of Boeing (BA) from Hold to BUY and increasing our price target to $275. Our upgrade is based on three factors: 1) the MAX return to service; 2) the improved outlook for travel and the airline recovery, which will correspond with a positive inflection in the aerospace cycle; and 3) the stabilization in the wide-body outlook. While we continue to see risk to the Boeing 737 MAX production schedule, we believe the combination of a recovery in passenger traffic, higher fuel prices, and improved airline financial health will support BA’s MAX delivery plans."

Herbery also noted that in his opinion, the fourth quarter of 2020 will prove to be the order trough for Boeing, which is in-line with the above sentiment expressed by Whitman.

Disclosure: Nicholas Ward does not have a position in Boeing. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Apple Continues Record Results Trend

Apple’s most recent quarter included a top and bottom-line beat, several records when it came to sales figures and user engagement metrics, and more than $30 billion in shareholder returns. Yes, you read that right...in just one quarter, Apple returned more cash to its shareholders than the vast majority of the companies in the S&P 500 produce in sales during an entire year. And, Mathew Fox of MSN believes that Apple’s generous trend is likely to continue.

The recent sell-off that we’ve seen in the market due to rising rates in the U.S. bond market has hit tech stocks extraordinarily hard. To a certain extent, this makes sense. As rates go higher, we should see adjustments to the risk premiums that investors are willing to place on equities.

This means multiple contractions across the equity space, and especially amongst those stocks trading with the highest and most speculative valuations. However, when pouring through Nobias’s data and reading analysis that our 5-star contributors are publishing recently, it appears as though the market is beginning to throw the proverbial babies out with the bath water.

A perfect example of this is Apple (AAPL). Of the 5-star analysts that Nobias’s algorithm tracks, just 28.2% currently have a bearish outlook on the stock. Yet, as of today’s $120.13/share, Apple shares are down more than 17% from the all-time highs that they set in late January.

Apple’s most recent quarter included a top and bottom-line beat, several records when it came to sales figures and user engagement metrics, and more than $30 billion in shareholder returns. Yes, you read that right...in just one quarter, Apple returned more cash to its shareholders than the vast majority of the companies in the S&P 500 produce in sales during an entire year. And, Mathew Fox of MSN believes that Apple’s generous trend is likely to continue.

In a recent article, Fox put a spotlight on Apple’s cash hoard, which totaled $196 billion at the end of its most recent quarter. Fox also touched upon the company’s recent $14 billion bond offering, which he believes the company will use to enrich shareholders further. “According to Bloomberg,” Fox says, “Apple's massive pile of cash on hand and $14 billion bond offering suggest the pace of shareholder returns from the company will likely rise to new highs this year.”

Regarding those record results, back on January 27th, Apple’s CEO, Tim Cook began the company’s fiscal first quarter conference call by saying, “We achieved an all-time revenue record of $111.4 billion. We saw strong double-digit growth across every product category, and we achieved all-time revenue records in each of our geographic segments.” Apple’s CFO, Luca Maestri, later continued to list records, highlighting all-time records from the company’s product and service segments, which posted year-over-year growth rates of 21% and 24%, respectively.

The top-line records resulted in bottom-line records as well. The $28.8 billion in net income (which was up 29% y/y) and the $38.8 billion of operational cash flows (which was up 26.7% y/y) were both all-time records for the company as well.

Iphone sales of $65.6 billion was an all-time record. Worldwide, Apple’s iPhone installed base is now above 1 billion active phones, which is a new record. Apple’s high margin service segment produced $15.8 billion in sales, which too, was an all-time record.

Apple’s total number of paid subscriptions continues to rise as well, making all-time highs each quarter recently as numbers increase on a sequential basis. The company had more than 620 million total paid subscriptions under its service category at the end of Q1, which was up more than 140 million (or 29.1%) compared to the same quarter one year ago.

Overall, Apple’s $111.4 billion revenue figure represented growth of 21%, year over year. Frankly, it’s astounding that the world’s largest company is able to continue to take market share and grow at such a strong, double digit clip.

For years, Apple bears have noted that the “Law of Large Numbers” would eventually result in this company’s growth stalling out. Well, Tim Cook and Co. have certainly debunked that thesis during the recent quarterly results. And, analysts widely believe that this trend is set to continue, with the current consensus estimate for Apple’s fiscal 2021 earnings-per-share growth rate to come in at 34%.

Yet, Apple isn’t immune to failure. For instance, Paul Ausick at 24/7 Wall Street, recently highlighted his belief that Apple, which was the world’s leader in the podcast distribution market in 2015, is likely to lose its crown to Spotify in 2021.

However, even if Spotify’s podcast listeners cross up above Apple’s current market leading position, it’s important to note that combined, the two companies will have a 48% market share, which still denotes a strong, defensible position for the company. What’s more, while it may be true that Apple is losing out to smaller, more nimbler competitors in certain areas of its business, the company continues to fire on all cylinders in the areas of the market with the highest annual sales potential.

Trevor Jennewine, of The Motley Fool, recently highlighted the company’s firm bucking of the “Law of Large Numbers” trend, stating that “Two years after becoming the first publicly traded $1 trillion company, Apple became the world's first $2 trillion company in August 2020.” He mentioned that at the end of 2020, Apple had more than 1.65 billion devices in use, globally. And, while this implies that the company may be approaching the edge of its addressable market share, in terms of hardware sales, bear who focus on this idea overlook the stickiness of Apple’s ecosystem, which means big revenues from company’s product refresh cycles, and more importantly, the company’s 2018 shift towards a more software oriented focus, which better monetizes its global installed base.

“Last year, Apple's services revenue was $53.8 billion, accounting for about 20% of total sales,” Jennewine notes. He goes on to highlight the recent heavy investments that the company has made into its services segment, highlighting the recent success of Apple Pay Apple Arcade, and Apple TV, and says, “In other words, as services account for a bigger portion of total sales, Apple should become increasingly profitable.”

Regarding Apple’s refresh cycle in 2021, Harsh Chauhan of The Motley Fool recently published a report titled, “3 Hot Stocks to Buy in a 2021 Market Crash” which calls for the record iPhone sales trend that we saw play out in the first quarter to continue throughout the entire year. Chauhan notes that famed Apple Analyst, Dan Ives of Wedbush Securities, “predicts that Apple could ship a record 250 million iPhones in 2021 -- surpassing the 231 million units it shipped in 2015 -- driven by the intense demand for the iPhone 12 models.” Chauhan says that “Ives' projection is based on the estimate that there are 350 million iPhones in an upgrade window, and the 5G-enabled offerings from Apple will kick off a massive upgrade cycle as consumers will want to make the jump to the new, much-faster, wireless standard.”

In a separate article which Chauhan published, titled “Why Apple Will be the Undisputed King of 5G Smartphones in 2021” he noted that Apple pulled ahead of rival Samsung, in terms of 5G phone shipments, during the recent quarter and he expects that gap to widen throughout the rest of this year. Chauhan says, “Third-party research predicts that Apple could command 35% of the 5G smartphone market in 2021.”

And, due to the massive potential of the global 5G transition, we’re not surprised to see Apple focus its energy on this trend, as opposed to smaller, less impactful ones, like market share in the podcast distribution space. Simply put, for Apple to continue to post strong growth with a $2.1 trillion+ market cap, the company is going to have to dedicate most of its energy towards mega-trends that can really move its financial needle.

This is why it appears that Apple is getting serious about entering into the automotive business.

Few industries can rival the global sales volume of the mobile phone space, yet with roughly 70 million cars sold on an annual basis during the last 5 years, the automotive segment could be the next industry that is ripe for disruption as the shift to driverless vehicles begins to play out over the coming decade.

Shanthi Rexaline, a Benziga staff writer with a 5-star rating at Nobias, says that after months of rumors floating around financial circles about Apple’s Apple Car ambitions, “It now appears the rumors could have some merit.” She cited a recent Bloomberg report which says that “Cupertino is in active discussions with several suppliers to procure the lidar technology that is used in self-driving vehicles.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

The Bloomberg report continued, saying that people familiar with the matter say that “After working on the Apple Car project for several years, Apple has now developed most of the necessary software, underlying processors and artificial intelligence algorithms that are needed.”

Rexaline highlights the importance of the driverless/electric vehicle market, saying, “EVs are considered the future in mobility, and this has prompted even traditional automakers to plunge headlong into these green energy vehicles.” She continues, saying that it comes as no surprise that the “Apple Car project is picking up steam after being in the works for several years now. Apple's products are known for their disruptive potential. Additionally, the company's design focus could make its EV offering an exciting one, despite it being late to the party.”

Disclosure: Nicholas Ward is long Apple. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Microsoft: A good time to invest?

Although Microsoft shares have not been isolated from the recent sell-off in the NASDAQ, with its share falling roughly 6.5% during the last week, there’s do doubt that sentiment is positive when it comes to the long-term prospects of this company. 70.3% of the reports we analyzed carried a bullish opinion. And, a prevailing theme amongst those articles was that the size and scope of Microsoft’s operations make this a stock that can fit into a wide array of investment strategies, meaning that there are very few limitations on the types of buyers who would be interested in owning MSFT stock.

In today’s world there are many viable strategies that financial managers adhere to when it comes to creating and protecting wealth for their clients. Investors and economists alike have debated the viability of various investment philosophies over the years and the truth is, there is no consensus as to which one of the myriad of methods of investing that we see employed in today’s market is the absolute best. This is the beauty of the market; success can be found in any ways, shapes, and forms. Yet, one of the most common phrases you will hear when listening to discussions about portfolio management is “diversification”.

This is a core concept of modern investing that helps to spread risk around, providing investors with exposure to a multitude of asset classes and asset types which come together to form a broader basket that have the potential to perform well, regardless of the broader economic environment and sentiment facing the market.

Within the equity space, specifically, you’ll often hear about different sector and industry allocation targets within a well diversified portfolio. You’ll also hear discussions about different subsets of equities, such as growth stocks, value stocks, defensive stocks, dividend stocks, etc. All of this can be intimidating.

Truth be told, the variety that exists in the market leads to another common phrase that we hear, which is “paralysis by analysis”, meaning that oftentimes, when faced which such a wide variety of options, investors freeze up, fail to capitalize on attractive opportunities that the stock market provides, and ultimately underperform.

However, all of this discussion about diversification leads us back towards one of the most talked about stocks in the market today: Microsoft (MSFT).

In recent days there have been dozens of articles, blog posts, and analyst reports published concerning this company. And, as our algorithm broke down the data, we found a consensus forming amongst 4 and 5-star analysts within the Nobias tracking system. Although Microsoft shares have not been isolated from the recent sell-off in the NASDAQ, with its share falling roughly 6.5% during the last week, there’s do doubt that sentiment is positive when it comes to the long-term prospects of this company. 70.3% of the reports we analyzed carried a bullish opinion. And, a prevailing theme amongst those articles was that the size and scope of Microsoft’s operations make this a stock that can fit into a wide array of investment strategies, meaning that there are very few limitations on the types of buyers who would be interested in owning MSFT stock.

Why is there such broad demand for shares of this $1.79 trillion company?

Well, as Wayne Duggan, a 5-star Nobias analyst who contributes to InvestorPlace put it in his recent article “4 Reasons To Love Microsoft Stock” this company benefits from secular growth in multiple ways. First and foremost, Duggan highlights the double digit revenue growth that Microsoft is generating with its cloud services. During Microsoft’s most recent quarter, the company’s “Intelligent Cloud” segment posted sales of $14.6 billion, which beat analyst estimates of $13.75 billion anad represented a year-over-year growth rate of 23%. Microsoft’s Azure cloud platform saw revenue growth of 50% during the quarter, which was an acceleration compared to the 48% growth during the prior reporting period. This strong cloud growth helped to propel the company’s overall revenue growth to 17% during the quarter.

But, as Duggan puts it, it’s not just about top-line growth. He says: “But all revenue is not created equal. Azure’s revenue is the good kind of revenue. Not only does Microsoft’s cloud sales have higher margins than its overall business, but the unit’s margins are expanding over time. As cloud revenue accounts for more and more of Microsoft’s overall revenue each quarter, it raises Microsoft’s overall profitability.”

And, speaking of demand that creates a situation where not only sales, but also prices rise (which translates into attractive margins), Duggan points out that Microsoft’s Office 365 subscriptions grew 15% on a year-over-year basis last quarter, while posting an average sale price that was 5% higher as well. Duggan quoted John Freeman, a Microsoft analyst at CFRA, who said, “Office, ~22% of [total] revenue, [is] benefiting from a cloud shift tailwind kicking in now that Office 365 cloud subscriptions are 2x+ license/support revenue,” Freeman says. CFRA is projecting Office 365 will help Microsoft more than double its 2019 EPS by 2023.”

The next major secular growth theme that Microsoft benefits from is gaming. The gaming industry has been on the rise for years now as technology in the space progresses; however, during the COVID-19 pandemic, social distancing, which bolstered the stay-at-home economy, has turned digital gaming into one of the world’s premiere segments of the border media/entertainment market. And, as Duggan Points out, Microsoft offers investors a leadership position in this industry, with its Xbox platform. Duggan notes that Microsoft has acquired 6 different gaming studios in recent years and the company’s Xbox Game Pass subscription service now has more than 18 million members. “In fact,” he says, “Microsoft reported 3 million new subscribers in its most recent reported quarter alone. Xbox’s content and services revenue was up 40% year-over-year in the quarter.”

And lastly, we arrive at social media, which is an industry that Microsoft entered in 2016 with its $26.2 billion acquisition of LinkedIn. Unlike other social media platforms, which have been mired with social and political headwinds, LinkedIn, which focuses purely on enterprise communications, has provided Microsoft with less volatile exposure to the growing market. Duggan says that “the platform has become a business-to-business marketing hub, and LinkedIn’s talent solutions (recruiting) business is now a major revenue source.”

What’s more, Duggan expects that LinkenIn will continue to provide Microsoft with opportunities to upsell users its enterprise software solutions. He notes that LinkedIn generates more than double the average revenue per user (ARPU) than peers Twitter (TWTR) and Snap (SNAP).

And, it appears that Microsoft’s appetite for social media exposure has not yet been satiated. Recent reports have risen regarding rumors that Microsoft management has held talks to acquire Pinterest (PINS). Danny Vena of The Motley Fool recently reported that while talks here have reportedly stalled, it’s clear that Microsoft is interested in the space.

Vena notes that Microsoft expressed interest in taking over TikTok’s U.S. operations last year when the Trump administration threatened to ban the app domestically due to digital security concerns. He goes on to say, “It's easy to see why Microsoft might be interested in adding another top-flight social network. Since acquiring LinkedIn, estimated revenue from the professional networking app has nearly quadrupled to more than $8 billion in 2020, though Microsoft doesn't break out its results.”

The primary concern that Duggan brings up is Microsoft’s valuation. He says that “Microsoft stock trades at 34.7 times the company’s trailing earnings and 31.75 times its forward earnings.” This ~35x blended price-to-earnings multiple is well above MSFT’s 20-year average P/E ratio of 21.1x. Yet, the high growth and similarly high margins associated with Microsoft’s growing software-as-a-service (SaaS) business appear to justify the high premium in analysts' eyes.

Duggan concludes his article, saying, “Now may not be the best time to buy MSFT stock for a quick trade. However, long-term investors who buy any dips can sleep well at night.” Duggan’s colleague at InvestorPlace, Dana Blankenhorn, who also happens to be a 5-star Nobias analyst, recently covered Microsoft’s cloud success as well, saying, “Microsoft’s global cloud is now a fully realized profits juggernaut.”

Yet, Blankenhorn also noted MSFT’s high valuation, saying “as the market turns toward value Microsoft doesn’t provide it. The price to earnings ratio is near 35x. A 56 cent per share dividend that once seemed generous now yields less than 1%.” But, much like Duggan, even with his valuation based caution in the short-term, Blankenhorn maintained a long-term bullish outlook, saying, “All 23 following it on Tipranks have it on their buy lists. Their average one-year price targets are 21% ahead of where it’s currently trading. You can buy Microsoft “on the dip” and look good in five years. I’m not selling my little stake.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Other analysts share a similar opinion. For instance, Billy Duberstein, of the Motley Fool, recently highlighted Microsoft in his article “Got $5000? 3 Tech Stocks To Buy And Hold For The Long-Term”. Duberstein touched upon Microsoft’s growth rates in the cloud and gaming segments and then he highlighted the company’s bottom-line success, saying, “Even more impressive, margins expanded, with operating income up 29% and earnings per share up 34% year-over-year. Even at an expensive-looking 34 times earnings, Microsoft's 34% EPS growth still gives it a PEG ratio of 1, which could actually be considered cheap!”

The most cautious stance that we came across from within the 5-star Nobias community, was published by David Van Knapp of Daily Trade Alert. However, even while presenting a cautious approach due to valuation, he still called Microsoft his “High Quality Dividend Growth Stock Of The Month” saying: “This month’s pick, Microsoft (MSFT), is in pretty much the same boat. Its rich valuation means that I would not recommend its purchase at the moment for most investors.

That said, some investors, especially younger ones, may not care much about current valuations, because in 10-15 years, they won’t care what they paid for the best companies; they will just be glad that they own them.”

Disclosure: Nicholas Ward is long shares of Microsoft. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Amazon beats expectations but Bezos exits

Amazon (AMZN) has been one of the most talked about stocks on Wall Street in recent weeks, due in large part to the big news that broke back in early February centered around the company’s famed founder and CEO, Jeff Bezos, stepping down from his current leadership role.

Since that news broke roughly a month ago, Amazon shares have fallen nearly 6%. Furthermore, Amazon shares are down roughly 10% from the highs in the $3,552.25 that they made roughly 6 months ago. This share price weakness also plays into the interest in the company. For years, Amazon has been one of the fastest growers in the stock market and when change happens, investors wonder if a company is losing its luster.

Anytime there is a leadership change at a founder-led company, investors get nervous. Such changes have come with turmoil in the past. However, this isn’t always the case and when we aggregated the opinions provided in articles written by analysts with a 5-star rating at Nobias, we saw that the outlook on Amazon shares continues to be bullish.

Amazon (AMZN) has been one of the most talked about stocks on Wall Street in recent weeks, due in large part to the big news that broke back in early February centered around the company’s famed founder and CEO, Jeff Bezos, stepping down from his current leadership role.

Since that news broke roughly a month ago, Amazon shares have fallen nearly 6%. Furthermore, Amazon shares are down roughly 10% from the highs in the $3,552.25 that they made roughly 6 months ago. This share price weakness also plays into the interest in the company. For years, Amazon has been one of the fastest growers in the stock market and when change happens, investors wonder if a company is losing its luster.

Anytime there is a leadership change at a founder-led company, investors get nervous. Such changes have come with turmoil in the past. However, this isn’t always the case and when we aggregated the opinions provided in articles written by analysts with a 5-star rating at Nobias, we saw that the outlook on Amazon shares continues to be bullish.

In his recent article, “Why Is Everyone Talking About Amazon Stock”, John Ballard, of The Motley Fool, highlighted the fact that while Amazon’s share price may be suffering, its operations and the underlying fundamentals that they generate certainly aren’t. When discussing the company’s recent fourth quarter report in a recent article, he said, “The first thing that jumps out about Amazon is that, while it's a large business, it continues to grow like a small one. In 2020, sales accelerated to a 38% growth rate, up from a still-robust 20% growth rate in 2019. And there isn't any sign that this momentum is waning.”

He then went on to showcase some of Amazon’s most appealing operational systems, saying, “One of Amazon's biggest advantages over the competition is logistics. At the end of 2020, the company had a massive 390 million square feet of fulfillment facilities and data centers. That's more than double its square footage in 2017. Management reported during its fourth-quarter earnings call that its square footage grew about 50% during the last year.” He continued, highlighting the long-term profits generated by the company’s ongoing investment into logistics infrastructure, explaining that, “Once a new fulfillment center is built, there's limited extra expense to keep it running, which means more incremental sales can be converted into a profit. This explains why the acceleration in sales during the holiday quarter contributed to a whopping 77% increase in operating income.”

Ballard then notes that the majority of Amazon’s value comes not from the retail business that the company is most famous for (the “everything” store which is Amazon.com), but instead, the company’s Amazon Web Services (AWS) segment and the broader ecosystem of apps and services that the company has built into its Amazon Prime subscription. He says that in 2019, he saw an analyst estimate the “value of AWS alone at $500 billion”. Ballard points out that this report was published in 2019 and since then AWS has continued along its strong, double digit growth trajectory, meaning that today, the value attached to AWS is likely even higher. He also mentioned a report that he read in 2020 by Needham analyst, Laura Martin, which estimated “that Amazon's media assets -- including Prime Video, Prime Music, and Twitch, the popular video game streaming site -- were worth another $500 billion.”

Today, Amazon’s total market cap is $1.56 trillion, meaning that these non-eCommerce related assets potentially make up the majority of Amazon’s value. Jason Hall, also of The Motley Fool, agrees with Ballard’s high level premise. In a recent podcast episode centered around Amazon’s Q4 results and the news that Bezos was stepping down, Hall said, “I think I said that most people, even a lot of investors, view Amazon through the lens of Amazon.com, through that retail business. It drives most of the revenues and it's how most people know about the company. The lens that Amazon's management views the company is through AWS [Amazon Web Services].”

And, with this in mind, he was bullish on the hire of Andy Jassy as Jeff Bezos’ replacement as CEO of Amazon, due to Jassy’s former job at the company as CEO of Amazon Web Services. Regarding Jassy, Hall says, “He has an MBA. He came in as, I think, a marketing manager. This is not an engineer, this is not somebody that came through writing code. This is somebody that started out with a more business-centric view of Amazon.”

During that same Motley Fool podcast, 5-star Nobias analyst, Danny Via, built upon this viewpoint, saying: “Jassy has been the CEO of Amazon Web Services and he is now taking the helm at Amazon, I think what you're going to see is his focus has always been on AWS. I think he probably has some big ideas about ways that AWS could further be used to enrich Amazon.” Via continued, “He's got that mindset. Coming from AWS, he's going to bring that perspective to the larger picture of how Amazon is run and we saw that happen with Satya Nadella and with Microsoft and how much Microsoft has benefited from that forward-looking perspective on cloud computing.”

For reference, since Satya Nadella took over from Steve Ballmer as CEO of Microsoft in February of 2014, Microsoft’s share price has risen from roughly $38/share to $236.94/share, representing gains of nearly 525%.

Right now, the average price target on Amazon shares provided by analysts with 4 and 5 star ratings in the Nobias system is $4077.33, which represents near-term upside potential of 29.5%. This is a far cry from the massive gains that Microsoft produced in the years after Nadella took over; however, roughly 30% gains by a $1.5 trillion company would be an impressive feat, nonetheless.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

But, the bull thesis surrounding Amazon isn’t just a short-term bet. 5-star Nobias analyst, Divya Premkumar, of The InvestorPlace, notes that Amazon just “Reported its best earnings yet and provided guidance for greater growth in the next quarter. According to analysts, there will be a sequential increase in earnings with earnings per share (EPS) going as high as $121.65 by 2024.”

Looking at AMZN’s valuation multiple in the market today, we see that shares are trading with a blended price-to-earnings ratio of 73.5x. And, while a 73.5x multiple might seem expensive to investors, Ballard points out in another recent article of his, that this premium is not all that elevated, relative to Amazon’s competition in the growing eCommerce space.

For instance, he notes that “Compared to other top e-commerce stocks, such as Etsy and Shopify, the online retail giant offers relatively good value. Amazon is cheaper based on price-to-sales and price-to-earnings ratios, and is No. 2 among the three when valued on free cash flow.”

It’s also worth noting that Amazon’s current premium is far below the company’s 5 and 10-year average price-to-earnings ratios of 103.7x and 187x multiples. And, even if Amazon shares continue to trade with today’s relatively discounted premium over the next 3 years and the above EPS estimate that Premkumar highlights comes to fruition, we’ll be looking at a share price of $8941, which would imply a 29.8% CAGR over the coming 4 years.

This is the type of performance that is likely to make any portfolio management happy, which is why Ballard concluded his recent article titled, “Why Is Amazon’s Stock So Expensive” by saying, “With so much opportunity ahead in e-commerce globally, Amazon remains a top growth stock to consider.”

Disclosure: Nicholas Ward is long Amazon. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Speculative Valuation Results in Tesla's Share Price Volatility

Tesla trades with a blended price-to-earnings ratio of 269.33. This implies that the market is pricing in major growth over the long-term. However, valuations that are based upon expectations that lie so far out into the future are highly speculative, which creates volatility in share price movement. And speaking of volatility, Luke Lango, Senior Investment Analyst at InvestorPlace, who receives a 5-star ranking by Nobias for his work, recently highlighted Tesla’s outperformance. He said, “At the start of 2020, this was a $90 stock. Recently, the TSLA stock price peaked at $900. In essence, then, Tesla stock has increased by 10X in just 14 months.”

Throughout its history, Tesla (TSLA) and its controversial CEO, Elon Musk (who, up until very recently, was the richest man in the world), have been at the center of a tug-of-war between value oriented and growth oriented investors.

Tesla has no shortage of doubters, with investors and analysts alike questioning the company’s growth strategy, capital allocation, and most frequently, the stock’s valuation. However, the stock’s performance speaks for itself, with the company’s market cap currently sitting at $712 billion.

Tesla, which is best known for its cutting edge technology, has not proven itself capable of producing reliable profits. Throughout its operational history as a publicly traded company, Tesla has posted negative earnings-per-share results more often than it has positive ones.

From 2010-2012 and then again, from 2015-2018, Tesla produced negative earnings-per-share. In 2019, Tesla’s annual earnings-per-share turned positive, at $0.01. In 2020, that annual figure rose to $2.24. And, peering into the future, the consensus analyst estimate for Tesla’s bottom-line results continue to rise higher, with analysts calling for 85% growth in 2021, 42% growth in 2022, and 22% growth in 2023. However, even with these double digit growth prospects in mind, many investors still have a hard time wrapping their heads around the triple digit price-to-earnings ratios that apply to this stock.

Right now, Tesla trades with a blended price-to-earnings ratio of 269.33. This implies that the market is pricing in major growth over the long-term. However, valuations that are based upon expectations that lie so far out into the future are highly speculative, which creates volatility in share price movement.

This Isn’t Your Grandfather’s Car Company

And speaking of volatility, Luke Lango, Senior Investment Analyst at InvestorPlace, who receives a 5-star ranking by Nobias for his work, recently highlighted Tesla’s outperformance. He said, “At the start of 2020, this was a $90 stock. Recently, the TSLA stock price peaked at $900. In essence, then, Tesla stock has increased by 10X in just 14 months.”

During this 14-month period, the S&P 500 (which Tesla joined in December of 2020) was up a comparatively smaller 21.6%. However, since making its all-time high in January, Tesla shares have experienced weakness. The stock is down 22.55% during the last month, and down approximately 13.6% during the last week alone.

Much of this negative volatility appears to be attributed to rising interest rates and the sell-off that the U.S. 10-year yield has inspired amongst high growth/speculative valued equities. However, Lango believes that these interest rate headwinds will prove to be temporary and taking a longer-term view, he says that this recent weakness in Telsa stock is going to prove to be a buying opportunity.

“You see… Tesla isn’t a car company. It’s an energy company. Tesla is figuring out to how harness clean energy and use to power the world,” Lango, who is known for his bullishness on innovation, notes that widespread use of Telsa’s energy storage technology could have helped to solve the recent power outage catastrophe that we saw play out in Texas.

“Indeed, in that world, no one loses power, anywhere, ever. Everyone is always powered.” Lango continues, “This is the future. And Tesla is at the epicenter of this future as one of the two leading companies in the energy storage space. Further, the company should be able to leverage its branding power — everyone knows the Tesla name and brand (and importantly, trusts it), while other players in this space are far from household names — to remain one of the largest player in energy storage for the foreseeable future.” Lango’s piece culminates in this bullish statement, “To that end, this dip in TSLA is a gift. Use it to buy the dip,” showing that not everyone is bearish when it comes to this company’s questionable fundamentals these days.

Tesla Makes Headlines By Adding Bitcoin To Its Balance Sheet

When tracking the 5-star analysts who cover Tesla, we’ve noticed that the company’s earnings statement and speculative growth prospects aren’t the only catalyst that is impacting TSLA stock. Recently, the company made big news with regard to its balance sheet with $1.5 billion investment in bitcoin. Much like TSLA shares, bitcoin has proven itself to be a very volatile and seemingly speculative investment. With this in mind, by tying itself to bitcoin in such a big way, Tesla’s management team has essentially accepted the volatility that comes along with digital currency.

Matthew Fox, a 5-star Nobias analyst who covers crypto-currency for Business Insider, recently covered Tesla’s big move into bitcoin. He noted that in a recent regulatory filing, Tesla said, "In January 2021, we updated our investment policy to provide us with more flexibility to further diversify and maximize returns on our cash that is not required to maintain adequate operating liquidity.”

Fox reports that in Tesla’s filing, the company said, "We may invest a portion of such cash in certain alternative reserve assets including digital assets, gold bullion, gold exchange-traded funds and other assets as specified in the future." This move away from cash is an interesting one, because traditionally, the U.S. dollar is seen as a conservative store of wealth. However, in a recent tweet, Elon Musk quickly summarized his rationale for moving into crypto, saying, “Money is just data that allows us to avoid the inconvenience of barter. That data, like all data, is subject to latency & error. The system will evolve to that which minimizes both.”

But, Musk’s company also acknowledges the risks that come with owning crypto. Fox’s reporting shows that such risk is discussed in the recent regulatory filing, with the company stating: "As intangible assets without centralized issuers or governing bodies, digital assets have been, and may in the future be, subject to security breaches, cyberattacks, or other malicious activities, as well as human errors or computer malfunctions that may result in the loss or destruction of private keys needed to access such assets." Yet, when it comes to investment markets, with risk comes reward. While some of Tesla’s recent sell-off has been attributed to bitcoin’s volatility, there are well known analysts who’re on board with companies placing bets on crypto.

Fox highlighted a recent note by famed Wedbush technology analyst Dan Ives, centered around Tesla’s move into bitcoin, which said, “This move could put more momentum into shares of Tesla as more investors start to value the company's bitcoin/crypto exposure as part of the overall valuation."

Tesla Isn’t Alone

Tesla isn’t the first big-tech company to adopt bitcoin as a cash alternative/investment/payment strategy. In October of 2020, Square made big news, purchasing 4,709 bitcoins, at an average cost of $10,617, for a total investment of $50 million. Fox also covered that announcement, highlighting Square’s statement: "Square believes that cryptocurrency is an instrument of economic empowerment and provides a way for the world to participate in a global monetary system.”

Fox noted that, “In 2018, it [Square] launched the ability to buy and sell bitcoins within its Cash app, and in 2019, the company formed Square Crypto, a team solely focused on open-source work in the crypto space.” In October of 2020, Square wasn’t the only digital payments company entering into the world of cryptocurrency. Paypal began to accept bitcoin as payment then as well.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

On the heels of that announcement, Ben Winch, of Business Insider, reported that billionaire investor, Mike Novogratz, came out with a bullish opinion on the move, saying that it was an “exciting day” for cryptocurrency and that, “All banks will now be on a race to service crypto. We have crossed the rubicon people." Tesla’s recent purchase appears to validate this idea. And, more recently, on February 23rd, 2021, Square added to its bitcoin holdings. The company purchased another $170 million worth of bitcoin, adding approximately 3,318 bitcoins to its collection, which when combined with its original 4,709 bitcoin purchase, now represents roughly 5% of the company’s cash position.

Conclusion

It appears that big tech is normalizing the use of digital currency as a way to diversify their balance, and therefore, minimize risk. We’re still very early in this adoption phase. Only time will tell if there will be a more wide-spread transition into bitcoin throughout the corporate world. However, these moves by well known names such as Tesla, Square, and Paypal certainly go a long way towards legitimizing crypto and moving forward, it will be interesting (to say the least) to see whether or not these early adopters will ultimately be rewarded by investors.

Disclosure: Nicholas Ward is long Tesla. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Disney Bucks Market Trend And Rises To New All-Time Highs

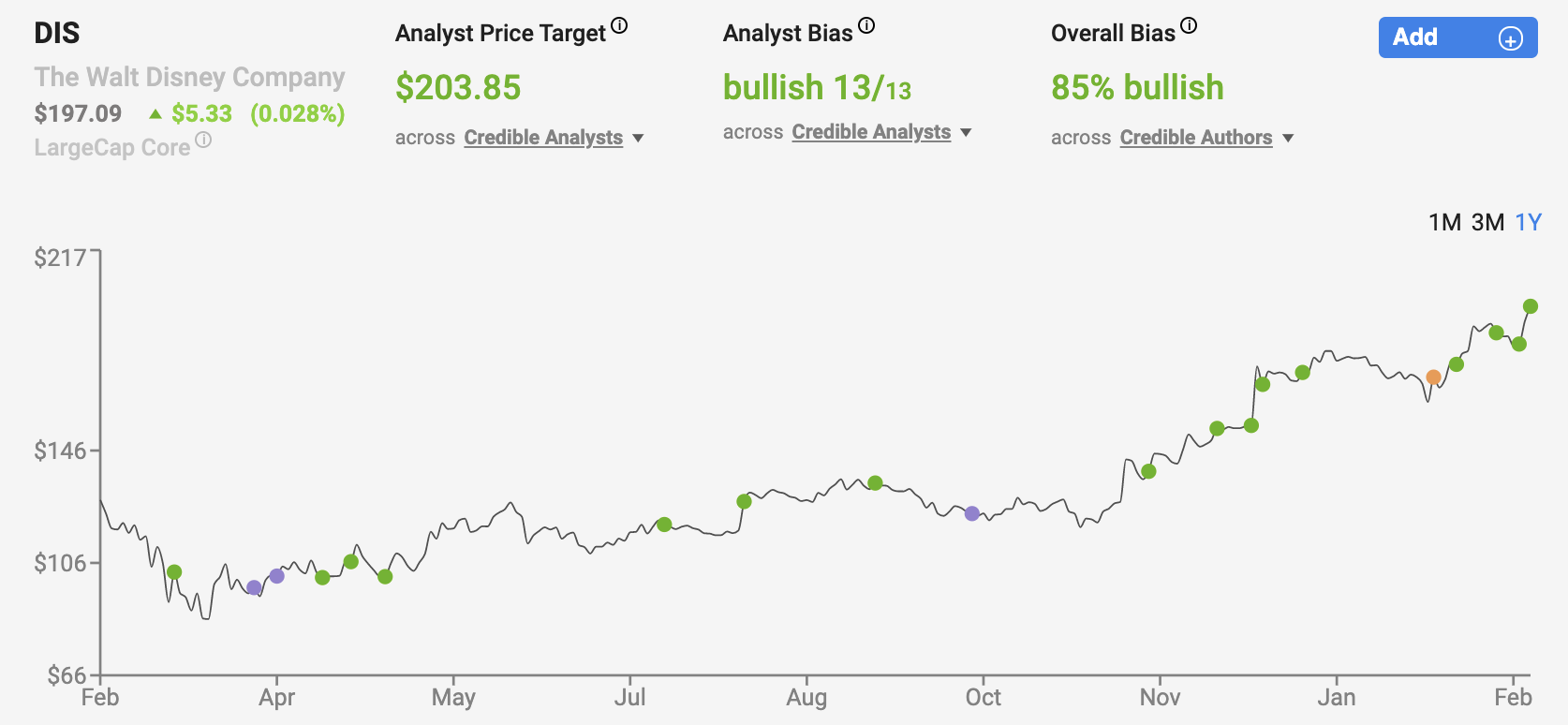

Disney’s share price appreciation during the COVID-19 pandemic period has led to an unprecedented valuation for the stock. Disney’s 5, 10, and 20-year average price-to-earnings ratios are 18.8x, 18.35x, and 21.5x. It’s clear that investors buying Disney shares at all-time highs here with nose-bleed multiples attached to them are placing confident bets on the long-term future of the company.

Yet, when looking at recent reports from the 5-star analysts that Nobias tracks, it becomes clear why there is such strong bullish sentiment behind Disney stock. Jason Hall, contributor at The Motley Fool, put it simply in a recent podcast, saying, “I've called Disney the best combination of a stay-at-home stock in a reopening stock all in one.”

After hitting all-time highs in mid-February, the broader markets have begun to sell-off a bit during recent trading sessions, due primarily to fears surrounding rising interest rates. During the last week, the Dow Jones Industrial Average (DJI) has traded relatively flatly, and sits just just a few tenths of a percent below its record highs. However, the S&P 500 (SPY) is down roughly 1.5% during the past 5 trading sessions and the more growth oriented and technology heavy NASDAQ 100 Index (QQQ) is down roughly 4.2%.

Many of the market’s top performers over the last several years are sought after growth stocks, yet these are precisely the names that are experiencing the most weakness right now because during a rising rate environment, stocks with higher price-to-earnings multiples are likely to suffer as the market re-prices risk and valuations contract.

Yet, in recent weeks, Disney (DIS) shares have bucked this trend and continue to trade higher while so many of the high flyers from the past 12 months have sold off. During the past week, Disney shares are up 5.76%, having hit all-time highs yet again on Tuesday. Year-to-date, Disney shares are up 8.78%. And, during the trailing twelve months, Disney shares have risen 41.82%, which is more than twice as much as the S&P 500, which is up 16.06% during the same period of time.

Although Disney hasn’t always been thought of as a growth stock by the market, it is receiving growth stock treatment by investors today because of the tremendous success of its Disney+ streaming platform. Disney shares currently trade for $197.09, which results in a blended price-to-earnings ratio of 97.96x. For comparison’s sake, this is higher than the 82.28x blended multiple that Disney’s streaming rival Netflix (NFLX) currently carries.

Disney’s share price appreciation during the COVID-19 pandemic period has led to an unprecedented valuation for the stock. Disney’s 5, 10, and 20-year average price-to-earnings ratios are 18.8x, 18.35x, and 21.5x. It’s clear that investors buying Disney shares at all-time highs here with nose-bleed multiples attached to them are placing confident bets on the long-term future of the company.

Yet, when looking at recent reports from the 5-star analysts that Nobias tracks, it becomes clear why there is such strong bullish sentiment behind Disney stock. Jason Hall, contributor at The Motley Fool, put it simply in a recent podcast, saying, “I've called Disney the best combination of a stay-at-home stock in a reopening stock all in one.”

Disney’s ability to satisfy the appetite of investors who’re looking for the strong performance of a “stay at home” stock and the strong upside potential of a “reopening” play puts it in rarified air (usually, these two investment theses are counter intuitive).

Sydnee Gateman of Gurufocus recently reported that the Yachtman Fund presented a very similar outlook in its recent shareholder letter, saying, “We believe the prospect of a recovery in the core businesses, combined with the growth of Disney+, positions the company well for the future.”

Joe Tenebruso, of The Motley Fool, agrees, having published an article titled on February 22, titled “Why Disney Stock Rose To An All-Time High Today”. In his article, Tenebruso comes to a similar conclusion as Hall and the Yacktman Fund, saying, “Its theme parks, cruise ships, and movie studios could see their revenues quickly rebound if the travel and entertainment industries experience a post-COVID boom. Meanwhile, its incredibly popular Disney+ streaming service will likely continue to fuel its growth during the remainder of the pandemic and in the years that follow.” Tenebruso concluded his piece, saying, “Investors seeking a relatively low-risk way to profit from an eventual return to normalcy would be wise to consider Disney.”

Disney+ Remains The Backbone Of Bullish Opinions

A common theme that we’re seeing here is a bullish focus on Disney+. The rise of Disney’s direct-to-consumer platform during the COVID-19 pandemic period has blown away analysts estimates and even Disney’s own internal projections. And, the pace of growth remains robust as Disney management has begun targeting international markets for future growth.