PYPL with Nobias technology: PayPal Shares Are Down 33% From Their 52-Week Highs. Is Now The Time To Buy?

Financial technology, or Fin-tech, stocks have been all the rage in recent years now due to the secular growth trend associated with the world moving forwards a cashless society driven by digital transactions. This has led to a slew of stocks in the fintech space experiencing massive rallies over the last 5 years or so. Paypal (PYPL) is an interesting story to follow in this space because up until very recently, it was a very popular stock to buy. PYPL shares are up 419% during the past 5 years. However, during the last month, they’ve fallen nearly 19%.

PayPal sold off after its recent earnings report and this weakness has pushed its year-to-date returns into negative territory. PYPL shares are down 11.06% on a year-to-date basis, underperforming the broader markets by a very wide margin (the S&P 500 is up nearly 25% throughout 2021 thus far).

Prior to PYPL’s recent earnings report, it was extremely easy to find credible authors highlighting the stock as a top growth pick. However, we wanted to take a look at what the credible authors that Nobias tracks have had to say about the stock more recently, to see whether or not this post-earnings dip is one that long-term investors should consider buying.

DISH Nov 2021

PayPal reported third quarter earnings results on November 8th, beating Wall Street’s consensus on the bottom-line, but missing expectations on the top-line. PayPal generated $6.18 billion of sales during Q3, which represented 13.2% year-over-year growth. However, this sales figure missed analyst estimates by $50 million and the 13.2% growth rate is the slowest that PYPL has generated since Q1 2020 (where the company generated 11.87% growth).

On the bottom-line, PayPal posted non-GAAP earnings-per-share of $1.11, which beat analyst estimates by $0.03/share. It’s worth noting that while PYPL’s top-line growth slowed during Q3, the reliable double digit sales growth that PYPL has been able to generate over the year is still the envy of just about every other company on Earth.

And, this isn’t a speculative stock that generates strong top-line growth that doesn’t translate to strong profits as well. PayPal split from Ebay (EBAY) in 2015 and since then the company has posted annual revenue growth results of 24% in 2015, 16% in 2016, 27% in 2017, 27% in 2018, 28% in 2019, and 25% in 2020. Right now, the analyst consensus points towards PYPL’s earnings-per-share rising by 19% in 2021, 14% in 2022, and 28% in 2023. In short, Wall Street believes that PayPal’s strong growth trajectory remains in place. With this strong fundamental growth in mind, it’s easy to see why analysts have bee largely bullish on PYPL stock over the years.

Looking at the credit authors that the Nobias algorithm tracks, there were several articles posted just before PYPL’s recent earnings report which highlighted the stock as a top buy pick. On October 27th, Trevor Jennewine, a Nobias 5-star rated author, published an article at The Motley Fool where he touted both PayPal and Zillow (ZG) as top picks.

With regard to PayPal, Jennewine said, “PayPal is one of the largest fintech companies in the world. Its platform spans 200 markets, offering a variety of financial services to both businesses and individual consumers. That includes payment processing (both in-store and online), point-of-sale solutions, and short-term financing for merchants; and mobile wallets, payment cards, shopping rewards, and crypto brokerage services for consumers.” “More importantly,” Jennewine continued, “PayPal is still growing its business in new directions.”

With regard to recent growth, he wrote, “In 2020, the company launched a variety of products, including the Venmo credit card and QR code payments for PayPal's mobile apps. Like its acquisition of iZettle in 2018, these moves expanded its in-store presence. And management has already reported strong momentum -- Venmo's revenue growth accelerated to nearly 70% in the most recent quarter, and roughly 1.3 million merchants now accept PayPal QR codes at checkout.” Jennewine believes that as PYPL adds more services to its fin-tech ecosystem, the company becomes more and more valuation to both merchants and consumers.

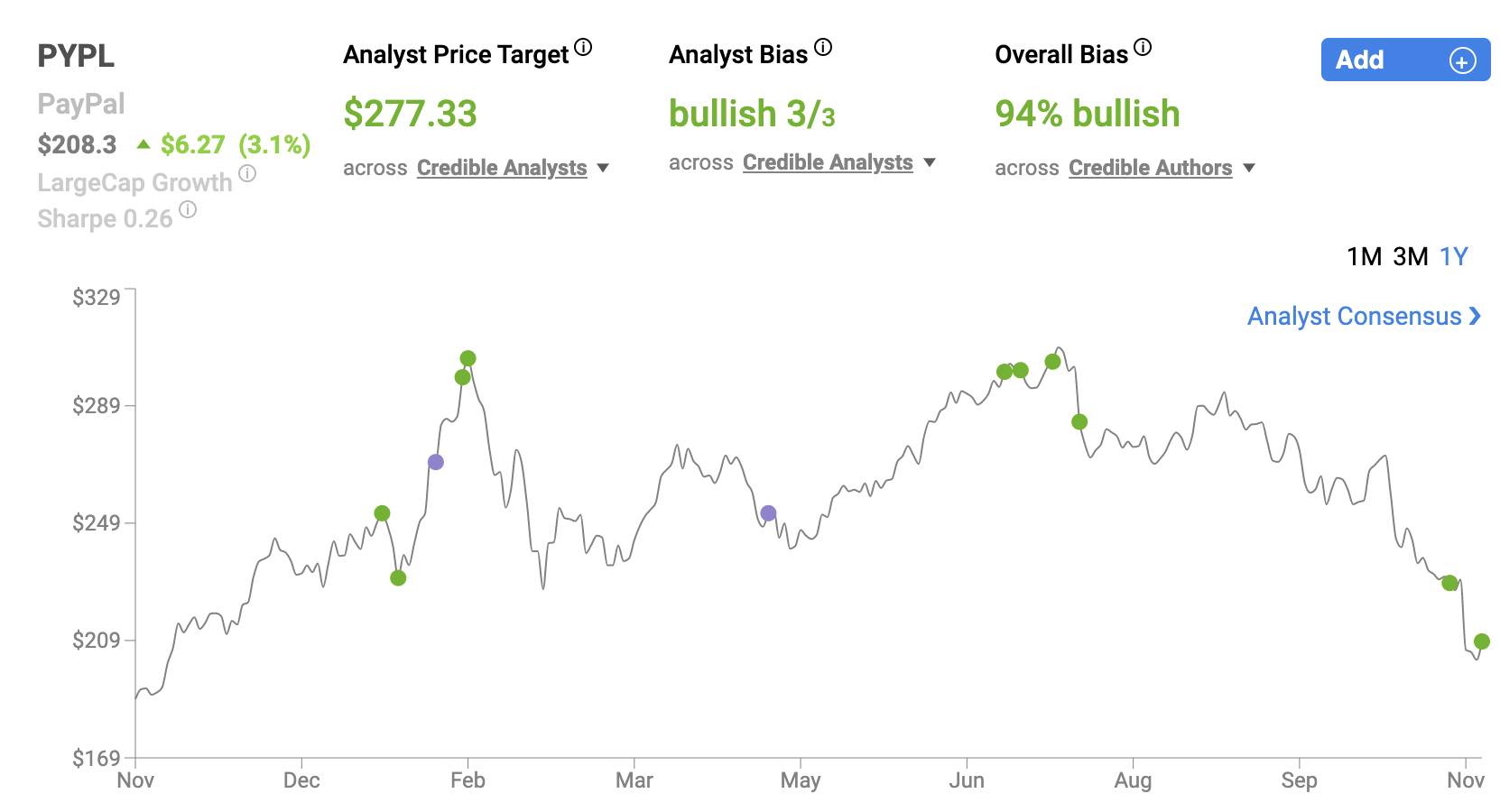

PayPal increased its active accounts by 13.3 million to 416 million at the end of Q3 and there appears to be a lot of room left to grow. Jennewine said, “The company currently puts its market opportunity at $110 trillion -- that figure is 90 times larger than the $1.2 trillion processed by PayPal's platform over the past year -- and management continues to execute on a strong growth strategy.” When he published his piece, he noted that PYPL shares were down 22% from their recent all-time highs and therefore, “That's why now looks like a good time to buy a few shares.” Today, PYPL shares trade for $208.30, which means they’re down nearly 33% from their 52-week high of $310.16. This implies that PYPL shares are an even better bargain today.

Neil Patel, another Nobias 5-star rated author, also published an article in late October highlighting PYPL as a top pick. Patel wrote, “Society is increasingly transitioning away from cash and toward digital payments, and PayPal is at the forefront of this movement. The company provides a broad range of tools for merchants to accept payments and for individuals with their daily financial lives. Over the past five years, the booming fintech has grown quarterly sales and profit 135% and 267%, respectively. And the stock has followed this strong fundamental performance, soaring almost six-fold during this time.”

He continued, saying, “A business wouldn't be great without the presence of a competitive advantage. In PayPal's case, it's powered by dominant intangible assets, including a strong brand and an innovative culture. The company is globally recognized as a leader in safety, security, and speed when it comes to payments, factors that can't be compromised.”

Patel highlighted PYPL’s strong second quarter margins and said, “And since the business already has the technological infrastructure in place to process massive numbers of transactions, the capital required to continue growing is minimal. PayPal invests 4% of sales in any period back into the company, which is why its free cash flow margin was a stellar 17% in the second quarter.”

During Q3, PYPL’s operating margin came in at 23.8%. Patel concluded his article saying, “These financial attributes, coupled with the company's consistent and steady revenue and profit growth over the past several years, support PayPal's forward price-to-earnings ratio around 47. The stock is also down more than 20% from its recent high in late July, giving investors a chance to buy on weakness.” Because shares have continued their sell-off since Patel published his piece, PYPL is even cheaper today.

Right now, PYPL trades for approximately 45.3x consensus 2021 earnings-per-share estimates of $4.60/share. And, on a forward looking basis, PYPL trades for roughly 39.7x the Wall Street consensus earnings estimate of $5.25 for 2022.

Vladimir Zernov, a Nobias 4-star rated author published a bearish article on the company after the recent Q3 results, explaining why PYPL shares fell 12% shortly after those results were posted. As Zernov notes, the bearish pressure was put onto the stock because of future guidance. He said, “In the fourth quarter, PayPal expects to report net revenue of $6.85 billion – $6.95 billion and adjusted earnings of $1.12 per share. The market is clearly disappointed by the soft guidance. Many analysts have already rushed to decrease their price targets for PayPal stock as they adjusted their models to account for slower growth.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Zernov touched upon the relatively valuation issue that PYPL shares face, writing, “The key problem for PayPal stock right now is that established competitors in the payments space like Visa (V) and Mastercard (MA) are trading at lower multiples. The valuation gap between PayPal and Visa/Mastercard has closed after the recent sell-off, but it is not clear why PayPal should continue to trade at a premium to peers if the company fails to meet growth targets.” He concluded saying, “In this light, there may be more room for multiple compression in PayPal’s case, which could push the stock below the $200 level.”

At the end of the day, the direction of PYPL’s share price is likely to follow its growth trajectory. This stock trades with a high valuation premium attached and as Zernov points out, the company is going to have to continue to execute on strong growth to justify that premium. Only time will tell if the company’s management team is able to reaccelerate growth into 2023 like Wall Street currently believes. But, in the meantime, we continue to see that the credible authors and analysts tracked by the Nobias algorithm remain bullish on PYPL shares.

When looking at the reports published by the credible authors that we track, 94% of them are “Bullish”. Wall Street analysts have had a week to digest PayPal’s Q3 report and the company’s revised Q4 guidance and update their price targets for PYPL shares. The blue chip (4 and 5-star rated) analysts that the Nobias algorithm tracks currently have an average price target of $277.33 on PYPL shares. Relative to the stock’s current share price of $208.30, this represents upside potential of approximately 33%.

Disclosure: Of the stocks mentioned in this article, Nicholas Ward is long PYPL, MA, and V. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.