Case Study: Amazon (AMZN) stock according to high performing analysts

Key Points

Performance

Amazon shares rose by 2.65% this week. On a year-to-date basis, Amazon shares are now up by 19.45%. This compares poorly to the S&P 500 which is up by 8.20% on a year-to-date basis thus far.

Event & Impact

Amazon’s CEO, Andy Jassy, published a letter to shareholders this week which focused on cost cutting, a return to strong profitability, and highlighted new growth plans in the artificial intelligence space.

Noteworthy News:

Jassy’s focus on profits provided peace of mind to investors who are worried about poor macroeconomic conditions. Jassy’s 2022 compensation was also highlighted, which came in much lower than previous years, and much lower than other big-tech CEOs, which highlighted AMZN’s determination to cut costs.

Nobias Insights

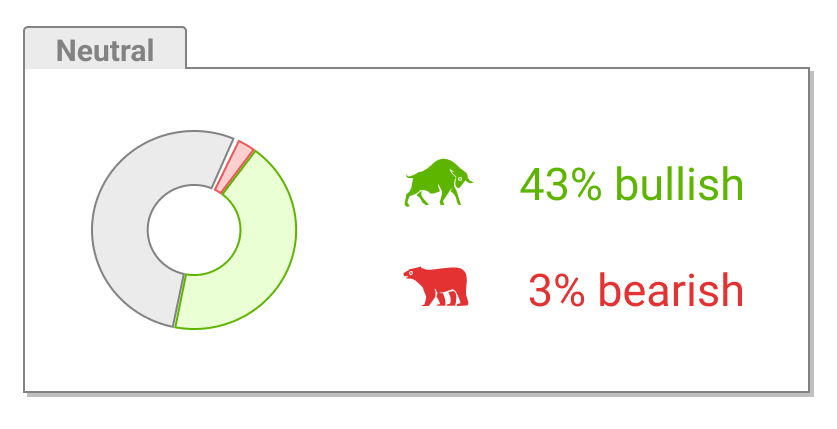

52% of recent articles published by credible authors focused on AMZN shares offer a “neutral” bias. However, six out of the six credible Wall Street analysts who cover Amazon believe shares are likely to rise in value. The average price target applied to AMZN shares by credible analysts is $148.17, implying upside potential of approximately 44.5% relative to the current share price of $102.54.

Bullish Take Nobias 4-star rated analyst, Mark Mahaney, stated, “The Amazon long thesis is "very much intact," with Amazon having a leading position in online retail, cloud computing and online advertising”.

Bearish Take Harsh Chauhan, a Nobias 4-star rated author, stated, “Amazon had a forgettable 2022 thanks to a tepid e-commerce market and a slowdown in the cloud computing business, which eventually led the tech giant to slash jobs from lucrative areas of its business.”

AMZN Apr 2023

For years, Amazon.com (AMZN) has been synonymous with successful big-tech growth. AMZN shares have risen by 687.95% during the last decade. This beats the broader performance posted by the S&P 500 and the tech-heavy Nasdaq Composite Index by a wide margin. In comparison, over the last 10-year period, these two indexes are up by 166.13% and 279.01%, respectively. And yet, the trailing 12-month period has been a tough one for Amazon.

Shares are down by 32.42% during the last year. Amazon’s growth slowed during 2022 and the company struggled to generate profits. However, the company’s CEO, Andy Jassy, published a letter to shareholders this week which addressed his plans to right the ship, which largely centered on cost cutting and profit generation.

Bearish Nobias Credible Analysts Opinions:

Nobias 4-star rated author, AJ Fabino, published an article at Benzinga this week which highlighted Jassy’s major talking points in his letter to shareholders. Fabino wrote, “Amazon.com, Inc AMZN CEO Andy Jassy addressed the company's short-term headwinds, continued investment in growth areas, cost control measures and generative AI in his annual shareholder letter Thursday.”

Fabino stated, “Jassy reaffirmed Amazon's commitment to investing in growth areas including AI, chip development and advertising, despite the cost-cutting measures — including layoffs — the company has undertaken.” “He confirmed that Amazon would shutter businesses lacking long-term potential, while allocating resources to promising enterprises,” Fabino continued.

Jassy focused on Amazon’s logistics segment, which continues to be a costly part of its retail business (as it turns out, it’s difficult to make money offering free 2-day shipping). In an effort to cut costs, Fabino said, “The company is transitioning from a national fulfillment network in the U.S. to a regional model to address rising costs and extended delivery times.”

Also, like so many other tech companies these days, Fabino noted that Jassy was bullish on artificial intelligence. Jassy made it clear that Amazon was competing in the AI market and it appears that shareholders were pleased.

Fabino said, “Jassy emphasized the transformative potential of large language models (LLMs) and generative AI in improving customer experiences across various applications.” “One of Amazon's LLMs, Titan, is already generating text for blog posts, emails and delivering search results on the company's website,” he added.

Overall, AMZN shares rose 2.65% this week, largely on the back of Jassy’s profit-centric letter. Huileng Tan, a Nobias 4-star rated author, also published an article this week that focused on Jassy’s letter to shareholders and made it clear that Jassy was putting his money where his mouth is, so to speak, when it comes to cost cutting.

Tan wrote, “Jassy was paid $1.3 million in 2022, including a $317,500 base salary plus another $981,000 in 401(k) plan contributions and security costs, according to the company's annual-proxy statement filed on Thursday.” She continued, “It's a massive drop from the $212.7 million he received in 2021 when he got promoted to CEO. Jassy's total compensation was $35.8 million in 2020.”

“In comparison,” Tan added, “Apple CEO Tim Cook received $84 million in total compensation in 2022, including bonuses and a $3 million base salary — although this may fall to $49 million in 2023. Microsoft CEO Satya Nadella was paid a total compensation of $55 million in 2022.”

Tan noted that in his letter to shareholders, Jassy mentioned that 2022 was "one of the harder macroeconomic years in recent memory."“Like many other tech companies, Amazon has been dealing with a downturn in the industry after business boomed during the pandemic. However, earnings are weakening amid fears of an impending recession,” she said.

It appears that lower CEO compensation resonated well with shareholders who understand that Amazon needs to cut costs and focus on generating profits during times like this. Harsh Chauhan, a Nobias 4-star rated author, mentioned Amazon is his bullish article titled, “2 Bargain Stocks on a Hot Rally to Buy Hand Over Fist Before They Soar Higher” that was published at the Motley Fool this week.

Chauhan said, “Amazon had a forgettable 2022 thanks to a tepid e-commerce market and a slowdown in the cloud computing business, which eventually led the tech giant to slash jobs from lucrative areas of its business.” He mentioned, “Revenue increased just 9% last year to $514 billion.” The company posted an adjusted loss of $0.27 per share as compared to a profit of $3.24 per share in the prior year,” he added.

“However,” Chauhan wrote, “2023 is expected to be a turnaround year for Amazon as far as its bottom line is concerned.” “The company's top-line growth is also expected to gather momentum, growing in the high single digits in 2023 and then in the double-digits from next year,” he said.

“For instance,” Chauhan added, “Amazon should benefit from easier comps in the e-commerce business in 2023.” “Meanwhile,” he continued, “global cloud infrastructure spending is anticipated to jump an impressive 23% this year, according to Canalys.”

Looking at the strength of Amazon’s cloud business, Chauhan said, “Amazon's 32% share of this market makes it the leader in the cloud infrastructure services space and puts the company on track to make the most of the solid growth opportunity available there.”

Furthermore, he noted that the company’s ongoing investments in the AI space have the potential to generate strong long-term growth for the company. “Mordor Intelligence estimates that the cloud AI market could grow at 22% a year through 2027, and Amazon's share of this market means that it could become a big beneficiary of this terrific growth,” Chauhan noted. Overall, he highlighted the stock’s relatively cheap valuation as a reason to buy shares on the recent dip.

Chauhan concluded his report by stating, “The stock is trading at just 2 times sales, a discount to the S&P 500's price-to-sales ratio of 2.4. So, investors are getting a bargain on this tech stock right now, especially considering the potential acceleration in its top and bottom lines.”

Bullish Nobias Credible Analysts Opinions:

Looking at the credible analysts coverage of Amazon, we see that it’s not just the credible authors who are bullish on AMZN shares. The most recent update that a Nobias credible analyst has provided on AMZN called for significant upside.

According to The Fly on the Wall, “Evercore ISI analyst Mark Mahaney lowered the firm's price target on Amazon.com to $155 from $160 based on a more conservative approach to the AWS segment and keeps an Outperform rating on the shares. The Amazon long thesis is "very much intact," with Amazon having a leading position in online retail, cloud computing and online advertising, but the firm's recent channel checks and forensic financial analysis suggest that AWS growth and margin stabilization "are not likely first half developments," the analyst tells investors.” Mahaney is a Nobias 4-star rated analyst.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

According to The Fly on the Wall, “Evercore ISI analyst Mark Mahaney lowered the firm's price target on Amazon.com to $155 from $160 based on a more conservative approach to the AWS segment and keeps an Outperform rating on the shares. The Amazon long thesis is "very much intact," with Amazon having a leading position in online retail, cloud computing and online advertising, but the firm's recent channel checks and forensic financial analysis suggest that AWS growth and margin stabilization "are not likely first half developments," the analyst tells investors.” Mahaney is a Nobias 4-star rated analyst.

Overall bias of Nobias Credible Analysts and Bloggers:

Overall, 52% of recent articles published by credible authors on Amazon have predicted that the stock will rise in value. This relatively neutral outlook differs significantly from the credible analyst outlook.

Currently 6 out of 6 credible Wall Street analysts that Nobias tracks who have offered an opinion on AMZN shares believe that they’re likely to rise in value.

Currently the average price target being applied to AMZN by these credible individuals is $148.17. Amazon shares currently trade for $102.54. Therefore, that credible analyst average price target implies upside potential of approximately 44.5%.

Disclosure: Nicholas Ward is long AMZN. Nicholas Ward wrote this article for Nobias at their request with the intention of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.