ExxonMobil: Can This Oil Giant Change Market Sentiment With Green Energy Proposals?

In recent years, ExxonMobil (XOM) has been a bit of a battleground stock for investors. For decades, this was a blue chip company known for generating strong total returns and paying out a generous and rising dividend yield. Some still argue that this is a best-in-breed type company; however, the company’s fundamentals would seem to imply otherwise. While it’s true that the energy industry as a whole has been out of favor for much of the last decade, XOM has seen its balances sheet deteriorate with its cash position dwindling, its cash flows trending towards negative growth, and its debt load rising as the company has been forced to do things like raise debt to sustain its high dividend yield.

The trouble that XOM has experienced is due to oil prices falling off of a cliff in 2014/2015. In January of 2014, crude oil was selling for more than $115/barrel. Well, by January of 2015, the price of a barrel of oil had fallen to below $40. There were investors who expected a quick bounce back from these record low prices, but the price of oil stagnated down in the $50-$70 range until early 2020.

In recent years, ExxonMobil (XOM) has been a bit of a battleground stock for investors. For decades, this was a blue chip company known for generating strong total returns and paying out a generous and rising dividend yield. Some still argue that this is a best-in-breed type company; however, the company’s fundamentals would seem to imply otherwise. While it’s true that the energy industry as a whole has been out of favor for much of the last decade, XOM has seen its balances sheet deteriorate with its cash position dwindling, its cash flows trending towards negative growth, and its debt load rising as the company has been forced to do things like raise debt to sustain its high dividend yield.

The trouble that XOM has experienced is due to oil prices falling off of a cliff in 2014/2015. In January of 2014, crude oil was selling for more than $115/barrel. Well, by January of 2015, the price of a barrel of oil had fallen to below $40. There were investors who expected a quick bounce back from these record low prices, but the price of oil stagnated down in the $50-$70 range until early 2020. And then, when the pandemic hit and global commerce and travel slid to a halt, energy demand fell down to unseen levels in the modern era, leading to oil prices down in the $20/barrel range, which is a price point that the industry hadn’t seen in roughly 70 years.

These low prices obviously didn’t bode well for XOM’s operations and this showed up during the company’s fundamental results throughout 2020. What’s more, Exxon has been forced to sell off assets and reduce its capital expenditures on things like exploration, leading analyst to fear that the company was doing long-term damage to its growth prospects. However, as the economy has begun opening up in recent months we’ve seen a renewed uptick in energy demand, causing the price of a barrel of oil to rise back to pre-pandemic levels in the $60 area. That is still well below the $100+ oil prices that we saw roughly 7 years ago; however, the increase has been like a breath of air for energy investors.

XOM recently reported Q1 earnings, in which it beat consensus analyst estimates on both the top and bottom lines. Exxon generated revenues of $59.15 billion, which was $2.16 billion higher than what analysts thought the company would produce, and represented 5.3% year-over-year growth. XOM also posted GAAP and non-GAAP earnings-per-share of $0.64 and $0.65/share respectively. The GAAP figure was $0.07/share ahead of analyst estimates while the non-GAAP figure beat the consensus number coming into the quarter by $0.05/share.

Most importantly, the company generated $9.3 billion in cash from operations, which meant that both capital expenditures made during the quarter, as well as the dividend, were covered by the company’s cash flows. This allowed Exxon to reduce its debt load by approximately $4 billion during the quarter. Regarding the uptick in cash flows, during Exxon’s first quarter report, CEO, Darren Woods was quoted as saying, “The strong first quarter results reflect the benefits of higher commodity prices and our focus on structural cost reductions, while prioritizing investments in assets with a low cost of supply.”

Overall, XOM was results from its upstream and downstream operations that beat analyst estimates; however, XOM shares still sold off on the news. This appears to be a bit of a classic “buy the rumor, sell the news” situation on Wall Street. Prior to the Q1 results, XOM shares were up roughly 42% of a year-to-date basis. This made the company one of the best performers in the entire market and it appears that investors needed to see even higher growth for the positive momentum to continue. And, as mentioned before, even though XOM’s cash flows were much higher in Q1 than they have been in the recent past, there is still concern amongst analysts that over the long-term, the secular headwinds that the fossil fuel industry faces will continue to present growth headwinds to an oil giant like XOM.

During recent years, we’ve seen other oil giants, such as British Petroleum (BP) and Royal Dutch Shell (RSD.A) discuss plans to reduce their energy emissions with ambitious carbon reduction goals. ExxonMobil joined this movement recently as well, making big news in the carbon capture space.

XOM’s CEO Woods touched upon this during the Q1 earnings report, saying, “We also made progress on our energy transition strategy by launching our new ExxonMobil Low Carbon Solutions business, which is initially working to develop innovative, large-scale carbon capture and storage (CCS) concepts, including the evaluation and advancement of more than 20 new opportunities, such as a multi-industry hub to reduce emissions from hard-to-decarbonize industries near the Houston Ship Channel. As the global leader in carbon capture, we are seeing growing public and private sector support for CCS as a critical enabling technology to reduce emissions and help meet society's net-zero ambitions.”

Our algorithm found a couple of articles written by 4-star Nobias analysts highlighting Exxon’s attempt to expand its renewable/”green” energy ambitions. Financial Buzz recently published an article highlighting a deal between ExxonMobil and Global Clean Energy’s biorefinery in Bakersfield, California. The author said, “Renewable diesel utilized Global Clean Energy’s camelina crop that may significantly reduce life-cycle greenhouse gas.

The president of ExxonMobil Fuels and Lubricants Company, Ian Carr, was quoted as saying, “Our expanded agreement with Global Clean Energy reinforces ExxonMobil’s longstanding efforts to support society’s ambitions for lower-emission fuels. Through our growing relationship, we remain focused on bringing renewable fuels to market that make meaningful contributions to help consumers reduce their emissions.” Financial Buzz said, “Analysis from California Air Resources Board data demonstrates that renewable diesel from no-petroleum feedstocks may provide life-cycle greenhouse gas emission reductions of 40 to 80% compared to petroleum based diesel.” These alternative fuels appear to be a growing part of Exxon’s plans, moving forward, as we continue to head into a future where there is increasing demand for environmentally friendly fuel sources.

Matthew DiLallo recently published this article on nasdaq.com, diving into the carbon capture plans that Woods discussed above. DiLallo said, “The $100 billion investment would capture the carbon emissions of refineries and petrochemical plants along the Houston Ship Channel, a key oil industry hub, and permanently store them underground. The initial phase, which Exxon could complete by 2030, would capture 50 million tons of carbon dioxide per year, the company says, roughly the equivalent of removing 11 million cars from the road.” DiLallo mentioned that in a recent interview with Politico,

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Woods touched upon his belief that “massive project” that Exxon is proposing is “the only realistic way for the U.S. to get anywhere near the kinds of quick, aggressive cuts to the nation's greenhouse gas output" that the Biden administration wants to see occur moving forward. DiLallo says that carbon capture technology is key to the future of the oil industry, noting that “It could enable the industry to deliver on its ambition of producing net-zero oil, where investments to reduce and capture carbon emissions would completely offset the emissions caused by the production and combustion of a barrel of oil.”

There has been push back amongst environmentalist who believe that energy executive and politicians alike should be focused on other energy sources that are truly emission-free; however, it’s going to take decades to wean the world off of its fossil fuel dependency so there appears to be a large opportunity for companies like Exxon to potentially profit from carbon capture and storage while technology innovation continues to occur that might lead towards more reliable and affordable alternative energy sources. DiLallo mentions that for the carbon capture system to work for companies, “governments would need to create the right financial incentives to make CCS projects economical, such as a cap-and-trade system or economywide carbon tax.”

Without financial incentives, it’s unlikely for these investments to offer attractive enough profits for large corporations to pursue them. Because of this, there is a lot of uncertainty surrounding Exxon’s large proposal and its long-term clean energy plans. DiLallo concludes his piece saying, “With the Biden administration currently seeking to set a clean energy standard instead, it's unclear if Exxon's proposed project will become a reality.” Because of this, investors aren’t likely to put a lot of weight on Woods’ grand proposal and therefore, it may be difficult for XOM to overcome the secular headwinds that the fossil fuel industry faces.

Disclosure: Nicholas Ward has no positions in any equity mentioned in this article. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

3M Company: Is The Recent Dip A Buying Opportunity?

The 3M Company (MMM) has been on quite a roll as of late. As 5-star Nobias Analyst, Lee Samaha noted in a recent article, the stock’s price rose more than 10% in the month of March. However, he notes, “There wasn't any major fundamental news in the month, so the stock price rise was likely caused by a change in investor sentiment.” And yet, this rally presents downside potential because anytime a stock rises on the back of bullish (and potentially greedy sentiment) as opposed to underlying fundamental growth, the risk of a pullback increases (due to the lack of a fundamental floor). Well, that’s exactly what we saw play out after 3M posted Q1 earnings this week.

When 3M reported its first quarter results, we saw the stock beat analyst estimates on both the top and bottom lines. MMM’s revenues totaled $8.9 billion during the quarter, which beat analyst estimates by $460 million and represented 9.6% year-over-year growth. The company’s sales growth was board based across its diverse product offerings. During Q1, 3M’s Safety and Industrial sales grew by 13.1%, its consumer brands posted 9.8% growth, and its healthcare segment posted 6.8% growth.

The 3M Company (MMM) has been on quite a roll as of late. As 5-star Nobias Analyst, Lee Samaha noted in a recent article, the stock’s price rose more than 10% in the month of March. However, he notes, “There wasn't any major fundamental news in the month, so the stock price rise was likely caused by a change in investor sentiment.” And yet, this rally presents downside potential because anytime a stock rises on the back of bullish (and potentially greedy sentiment) as opposed to underlying fundamental growth, the risk of a pullback increases (due to the lack of a fundamental floor). Well, that’s exactly what we saw play out after 3M posted Q1 earnings this week.

When 3M reported its first quarter results, we saw the stock beat analyst estimates on both the top and bottom lines. MMM’s revenues totaled $8.9 billion during the quarter, which beat analyst estimates by $460 million and represented 9.6% year-over-year growth. The company’s sales growth was board based across its diverse product offerings. During Q1, 3M’s Safety and Industrial sales grew by 13.1%, its consumer brands posted 9.8% growth, and its healthcare segment posted 6.8% growth.

he company noted that its growth was also strong across all geographic regions, with revenues rising by 18.1% in the Asia Pacific region, by 10.4% in the Europe, Middle East, and Africa region, and by 4.5% in the Americas region.

These higher sales led to positive growth on the bottom-line as well. The company’s earnings-per-share came in at $2.77 on a GAAP and non-GAAP basis, beating GAAP expectations by $0.50/share and non-GAAP expectations by $0.48.share. These two earnings-per-share results represented 23% and 27% growth, respectively, when compared to the company’s GAAP and non-GAAP earnings results from one year ago.

During Q1, the 3M company generated $1.7 billion in operating cash flow and returned $1.1 billion to shareholders ($858 million was paid in dividends and $231 million was dedicated to share buybacks). Looking at the Q1 report it appears that management was quite bullish. Here’s an excerpt from 3M’s press release regarding earnings: "The first quarter was highlighted by broad-based organic growth, robust cash flow and a double-digit increase in earnings per share," said Mike Roman, 3M chairman and chief executive officer. "Our four industry-leading businesses are delivering strong results, while we accelerate 3M's digital transformation and sustainability efforts with significant new goals to improve air and water quality. While uncertainty related to COVID-19 remains, we will stay focused on driving growth, building on favorable market trends, improving operational performance and delivering for customers and shareholders." However, the market did not agree. 3M shares fell roughly $10/share, from the $202 area to the $192 area, representing a 5% dip, on the heels of the Q1 earnings release.

The 3M company has been struggling to generate sustained growth for several years now. In 2018, the company’s full-year earnings-per-share totaled $9.98. During 2019 and 2020, MMM experienced negative bottom-line growth, due in large part to the U.S./China trade war and then the COVID-19 pandemic. In 2021, analysts expect to see a return to growth; however, even if 3M hits the current consensus growth estimate of 12% this year, its earnings-per-share will only total $9.77, still less than it was just several years ago. This turnaround process has been long and arduous. And, as Samaha, writes in a different piece than the one linked above, there is still a lot of uncertainty surrounding 3M’s stock.

In a recent article, previewing 3M’s Q1 prospects, Samaha said, “The good news is that the company has plenty of financial firepower to do so and is actively pursuing changes. The bad news: There's little hard evidence that the restructuring is having a significant impact, and the upcoming first-quarter earnings report on April 27 might confuse more than it clarifies.” Samaha touched upon the company’s recent struggles, saying, “Given weak end-market conditions in recent years, it's understandable if they have performed poorly. However, what isn't forgivable is that the less cyclical segments, namely healthcare and consumer, have disappointed the most.” However, even with the uncertainty clouding the stock’s growth outlook, Samaha is bullish on the company’s ability to generate strong profits, noting, “The company generates bundles of earnings before interest, depreciation, amortization (EBITDA), and FCF.”

What’s more, Samaha highlights the relatively cheap valuation that 3M trades with, relative to its peers. Just before earnings, 3M shares were trading with a 17.5x price-to-free cash flow multiple. With that in mind, Samaha says, “Its price-to-FCF valuation looks cheap, especially compared to a multi-industry peer like Illinois Tool Works, trading at nearly 28 times its FCF.” Due to its post-earnnigs dip, MMM is even cheaper now. With these strong cash flows and relatively cheap valuation in mind, Samaha says, “There is a strong case for buying/holding the stock, but management needs to start delivering in 2021, particularly in the healthcare segment.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

However, he noted that if the company doesn’t raise its guidance during the first quarter results, like he expects so many of MMM’s industrial peers to do in light of the recent broad economic resurgence, then shares would likely continue to languish. Well, during the Q1 report, MMM reiterated previously provided full-year 2021 guidance, calling for earnings-per-share to be in the range of $9.20-$9.70. MMM expects to see full-year sales growth of 5-8% with organic local-currency growth in the 3-6% range.

While sticking with guidance is certainly better than reducing it, it appears that the market was of the same opinion as Samaha, expecting a raise. 3M continues to face pressures related to pollution litigation, which David Trainer, a 5-star Nobias Analyst highlighted in a recent article as having a negative impact on the company’s financial results. This headwind, combined with the continued uncertainty around the company’s restructuring and ongoing tariff related headwinds associated with certain end markets (especially in the automotive space) are likely to continue to serve as hurdles for the stock to clear in terms of rising sentiment and a potential share price rally. However, when looking at the blue chip analyst community, the prevailing sentiment surrounding MMM is a positive one, pointing towards apparent upside potential.

There are 20 bullish ratings by 4 and 5-star rated Nobias analysts, compared to just 7 sell ratings. 3M is a dividend aristocrat, having increased its annual dividend for 63 consecutive years now. The company generates reliable sales and earnings, has a strong balance sheet, and a product portfolio that many of its peers are likely envious of. It appears that the high quality analysts we track believe that the company has what it takes to overcome its short-term issues, meaning that this is a dip that long-term investors may want to seriously consider buying.

Disclosure: Nicholas Ward is long MMM.. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

United Parcel Service Appears Benefit From Strong Secular Trends

It’s earnings season, which typically means an abnormal amount of volatility in the markets as new results and guidance rolls in. However, thus far during the first quarter reporting, we’ve seen relatively tepid share price movement, especially after strong beats and raises. This seems to imply that strong sales and earnings growth has already been priced into the market. And, this theory makes a lot of sense, being that we’re coming out of the COVID-19 recession and the re-opening of the economy should generate some of the best gross domestic product growth that the United States has seen in a very long time. However, there was one major exception to this trend this week. United Parcel Service (UPS) posted great numbers on Tuesday, which sent the stock soaring more than 11%.

UPS has made a habit of beating Wall Street estimates in recent quarters. After its Q4 results which were posted back in early February, Daniel Foelber, a 4-star Nobias analyst from The Motley Fool, highlighted the results saying, “The earning beat caps off a terrific year for the package delivery stock. Shares of UPS trounced the market last year, producing a 44% total return compared to the market's 17%.”

It’s earnings season, which typically means an abnormal amount of volatility in the markets as new results and guidance rolls in. However, thus far during the first quarter reporting, we’ve seen relatively tepid share price movement, especially after strong beats and raises. This seems to imply that strong sales and earnings growth has already been priced into the market. And, this theory makes a lot of sense, being that we’re coming out of the COVID-19 recession and the re-opening of the economy should generate some of the best gross domestic product growth that the United States has seen in a very long time. However, there was one major exception to this trend this week. United Parcel Service (UPS) posted great numbers on Tuesday, which sent the stock soaring more than 11%.

UPS has made a habit of beating Wall Street estimates in recent quarters. After its Q4 results which were posted back in early February, Daniel Foelber, a 4-star Nobias analyst from The Motley Fool, highlighted the results saying, “The earning beat caps off a terrific year for the package delivery stock. Shares of UPS trounced the market last year, producing a 44% total return compared to the market's 17%.”

It’s true that from October of 2020 through April 26th of 2021, EPS shares hovered in a relatively tight range, trading in the $170’s. And this may come as a surprise to many because as Foelber mentioned in his recent article, the company set many records during 2020. He said, “UPS earned a record-high $84.6 billion in revenue, up 14.2% year over year (YoY). Adjusted operating profit was $8.7 billion, up 7% YoY. Diluted adjusted earnings per share (EPS) finished the year at a record-high $8.23. And the company paid a record-high $3.6 billion in dividends. Its dividend now yields 2.5%.”

Foelber also hypothesized that what was holding back UPS shares moving forward was the unknown associated with whether or not the heavy investments that the company has made in the last few years with regard to expanding its logistics operations and attempting to make them more efficient would pay out. He said, “UPS's performance, and potentially its stock price, will depend on the effectiveness of last year's spending more so than this year's. UPS paid a hefty price to expand its faster shipping network and beef up its logistics to handle the vaccine rollout. The extent to which it can capitalize on those efforts could ultimately determine its growth over the next few years.” And, arriving at the Q1 results, it appears that the market totally underestimated UPS’s ability to capitalize on those investments and therefore, its overall growth potential in 2021.

The outsized volatility that shares posted after Q1 results this week caught the attention to investors, analysts, and commentators alike. UPS was one of the most publicized stocks this week, with the Nobias algorithm recognizing dozens of reports on the stock. And, with that in mind, we wanted to highlight the opinions provided by the highest quality analysts (only those rated 4 and 5-stars by the Nobias system) for readers who’re wondering what to make of the big move UPS shares.

During the first quarter, UPS posted revenues of $22.91 billion, which beat consensus analyst expectations across Wall Street by $2.17 billion and represented a 27% year-over-year sales increase. UPS’s Q1 earnings-per-share came in at $2.77 on a non-GAAP basis and $5.47 on a GAAP basis. These two figures beat the consensus Wall Street estimates by $1.05 and $3.79, respectively. This GAAP earnings-per-share result was up 393% year-over-year (and up 141% on an adjusted basis). The company’s consolidated operating profits totaled $2.8 billion, representing 158% year-over-year growth (and up 164% on an adjusted basis). During Q1, UPS saw average daily volumes increase by 14.3% year-over-year.

In the United States domestic segment, UPS’s sales increased by 22.3%, led by strength in small and medium businesses. The company’s average price-per-package increased by 10.2%, which led to higher margins for the segment, with operating margin coming in at 9.7% (domestic operating margin was up 10.4% during the quarter on an adjusted basis). Internationally, UPS’s average daily volume increased by 23.1% with led to revenue growth of 36.2%. The company said that its package volumes increased in all of its operating regions, though the big sales growth was driven primarily by strength in Asia and Europe. UPS’s operating margin came in at 23.6% for the international segment (up 23.7% of an adjusted basis).

United Parcel Service’s senior management came out incredibly bullish on the quarterly results. During the earnings report, the company’s CEO, Carol Tome’ was quoted as saying, “I want to thank all UPSers for delivering what matters, including COVID-19 vaccines. During the quarter, we continued to execute our strategy under the better not bigger framework, which enabled us to win the best opportunities in the market and drove record financial results.”

5-star Nobias analyst, Lou Whiteman, of The Motley Fool, was also bullish on the results, concluding the introduction of his recent UPS article by saying, “The company is seeing strong revenue growth across all segments and improving pricing power, leading to the beat.” To a certain extent, Whiteman noted that these stellar Q1 results were very predictable, because it was obvious that UPS was going to be a major beneficiary of the economic recovery since the pandemic lows.

When COVID-19 first struck during Q1 of 2020, the worldwide economy essentially shut down. And, when commerce stopped, the logistics space suffered. And yet, eCommerce was one of the big winners of the pandemic period, with consumers stuck at home and reluctant to venture out into the public. Shipping players like UPS benefited from eCommerce growth with higher business-to-consumer (B2C) volumes and now that the economy is reopening, its business to business (B2B) volumes have increased nicely as well.

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

There has been fear amongst investors that logistics players like UPS would not be able to sustain the growth related to the re-opening and/or the change of consumer habits during the pandemic related to eCommerce, and therefore, any near-term growth would appear to be isolated instead of secular. But, Whiteman is of the belief that UPS’s post-pandemic growth will be long lasting, saying, “With each passing quarter evidence is growing that UPS and its rivals are likely to be able to generate strong margins on the domestic business even after the pandemic recedes, thanks to strong demand, streamlined costs, and better asset utilization. Investors are understandably excited about this business.”

Sean Sechler, a 4-star Nobias analyst who writes for Entrepeneur.com, highlighted similar bullish sentiment in his recent article, saying, “While some investors might think that the uptick in e-commerce shipping was only a short-term boost driven by the pandemic, the truth is that e-commerce volumes have been increasing each year for a while now and that likely won’t be changing anytime soon.”

With this in mind, it appears that the investments that UPS management has made are proving to the well worth the costs. Without them, the company would not be in the situation that it is in today, able to take advantage of rising global shipping demand. In short, the risk incurred was certainly worth the reward and UPS investors are experiencing nice gains become of management’s foresight.

Disclosure: Nicholas Ward has no position in any equity mentioned in this article.. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Proctor and Gamble Just Raised Its Dividend for the 65th Consecutive Year

Procter and Gamble (PG) is one of the more interesting stocks in the consumer packaged goods space right now. It wasn’t all that long ago that this illustrious company was being beaten down by the market, due to its poor performance during 2015 and 2016 when the company posted back-to-back years of negative earnings growth (something that is very rare in the long-term history of this stock). This period sparked a significant restructuring of PG’s operations and brand portfolio, inspired by an ugly proxy fight between Procter’s management and Trian Fund Management, led by Nelson Peltz, a famous activist investor. At the end of the day, all’s well at that ends well in the activist investment world. Eventually Peltz was awarded board seats and the leadership shake up has served as a catalyst for the major turnaround of this mature stock. During its past 2 fiscal years, PG has posted double digit earnings growth. These days, the company’s operational growth puts it near the top of its peer group. However, while sales and earnings continue to grow nicely, the stock has still struggled year-to-date, creating an interesting opportunity for investors.

Procter and Gamble (PG) is one of the more interesting stocks in the consumer packaged goods space right now. It wasn’t all that long ago that this illustrious company was being beaten down by the market, due to its poor performance during 2015 and 2016 when the company posted back-to-back years of negative earnings growth (something that is very rare in the long-term history of this stock). This period sparked a significant restructuring of PG’s operations and brand portfolio, inspired by an ugly proxy fight between Procter’s management and Trian Fund Management, led by Nelson Peltz, a famous activist investor. At the end of the day, all’s well at that ends well in the activist investment world. Eventually Peltz was awarded board seats and the leadership shake up has served as a catalyst for the major turnaround of this mature stock. During its past 2 fiscal years, PG has posted double digit earnings growth. These days, the company’s operational growth puts it near the top of its peer group. However, while sales and earnings continue to grow nicely, the stock has still struggled year-to-date, creating an interesting opportunity for investors.

PG shares are down 3.7% year-to-date, which pales in comparison to the S&P 500’s 11.5% gains. This underperformance may seem odd to some, due to the fact that PG has posted two quarterly earnings results thus far during 2021, both of which have involved top and bottom-line beats, relative to analyst expectations. However, looking at the company’s valuation, we begin to see why there is a tug-of-war going on right now between the bulls who are focused on the company’s strong growth turnaround and the bears who say that shares are overly expensive.

Today, PG shares are trading with a blended price-to-earnings ratio of 24.2x attached to them. Looking at full-year earnings expectations for the company in fiscal 2021, we see a forward looking price-to-earnings ratio of 23.8x. Both of these figures are well above the stock’s long-term (20-year) average price-to-earnings ratio of 19.9x.

Touching upon potential overvaluation, 5-star Nobias analyst, The Individual Trader, recently posted an article on Seeking Alpha which explained this valuation scenario. They note that the company’s RSI is in decline after a strong top in the 90 range and said, “Shares actually presented a similar set-up back in 2017 when the share price of P&G continued to rise but momentum was once more faltering. This led to a 20%+ down-move in the share price in the space of four months which in hindsight presented an excellent long-term buying opportunity.”

The Individual Trader combined this technical set-up with some more fundamental analysis as well, saying, “Many investors may be waiting for this potential down-move to happen due to shares being perceived as being overvalued. The forward sales multiple of 4.57 as well as the forward book multiple of 7.11 definitely come in on the high side compared to the sector as well as P&G's historic averages. Nevertheless, P&G cannot be blamed for the market loving this company and we see plenty of evidence of this when we view the profitability metrics. EBIT margin of 24.13% as well as trailing operating cash flow of $19.03 billion are well above average for P&G and explains in part why shares have rallied well over 20% since March of last year.”

Valuation arguments are tricky to make. There are so many metrics in play that parties sitting on both sides of the bear/bull aisles can typically find data to justify their stances. Really, only with the benefit of hindsight, can we truly see the impact of valuation on share price movement. But, in the meantime, this company is doing all that it can to sway investor sentiment towards the bullish end of the spectrum.

During the company’s fiscal third quarter, PG’s net sales increased by 5.2%, totaling $18.1 billion. This $18.1 billion revenue figure beat analyst expectations by $150 million. During the quarter, PG’s organic sales growth came in at 4%. On the bottom-line, PG produced diluted net earnings per share of $1.26, which represented 13% year-over-year growth relative to reported earnings-per-share and 8% year-over-year growth relative to core earnings-per-share.

Charles Sternberg, a 4-star Nobias analyst who writes for Happi, touched upon PG’s segment results in a recent article. He said that the company’s Beauty segment posted 7% y/y growth, its Grooming segment posted 4% y/y growth, its Healthcare segment posted 3% y/y growth, its Fabric and Homecare segment posted 7% y/y growth, and its Baby, Feminine, and Family Care segment posted -1% y/y growth.

During the fiscal Q3 report, PG’s Chairman, President, and CEO, David Taylor, said: “We delivered another quarter of solid top-line, bottom-line and cash results in what continues to be a challenging operating environment. We remain focused on executing our strategies of superiority, productivity, constructive disruption and improving P&G’s organization and culture. These strategies enabled us to build strong business momentum before the COVID crisis and accelerate our progress during the crisis, and they remain the right strategies to deliver balanced growth and value creation over the long term.”

PG’s operating income came in at approximately $3.8 billion during the quarter, up 10% on a year-over-year basis. This strong bottom-line performance allowed the company to increase its dividend as well. 5-star Nobias analyst, Demitri Kalogeropoulos, recently highlighted PG’s dividend growth outlook in his article, “Two Dividend Giants To Buy Before Their Next Payout Hike”. In this piece, Kalogeropoulos highlighted PG’s strong sales growth, saying, “Organic sales jumped 8% in P&G's last outing and are expected to rise for the full year following a spike in fiscal 2020.” He then went on to highlight the company’s bottom-line success, saying, “P&G generated $10 billion of operating cash in the past six months, compared to $8.5 billion a year earlier.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Kalogeropoulos penned this piece in late March, before the recent dividend announcement. In his article, he said, that the company’s recent success “gives management the flexibility to announce a hike in April that should be at least as big as last year's 6% hike.”

Well, it turns out he was correct.

On April 13th, PG announced that it was increasing its quarterly dividend by 10%, raising the payment from $0.7907/share to $0.8698/share. This increase extends PG’s annual dividend increase streak to 65 consecutive years. And, if six and a half decades of annual dividend increases doesn’t impress you, then maybe this statement that the company made during its quarterly report will: “P&G has been paying a dividend for 131 consecutive years since it’s incorporation in 1890.” Regarding this amazing streak, Kalogeropoulos said, “That kind of streak is only possible because of its dominant hold on several consumer staples niches, including paper towels, detergent, and shaving care.”

It’s also worth mentioning that PG’s shareholder return story is not limited to its dividend growth. During the Q3 report, management said, “P&G expects to pay more than $8 billion in dividends in fiscal 2021. The Company increased its outlook for common stock repurchase from up to $10 billion to approximately $11 billion in fiscal 2021. Combined, P&G now plans to return about $19 billion of cash to shareowners in this fiscal year.” Capital return plans like this from a well established blue chip name is why PG remains one of the most widely owned stocks by hedge funds on Wall Street and a favorite amongst retail investors as well. So, while investors wait and see if the company’s share price will rebound throughout the remainder of 2021, they can rest assured that PG management will continue to be quite generous with its cash flows.

Disclosure: Nicholas Ward has no position in any equity mentioned in this article.. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Verizon: A Bull/Bear Tug-Of-War Between Dividends and Debt

Staying true to trend this week, the third company that we’re looking at, Verizon (VZ) is down on a year-to-date basis. This is interesting, because it wasn’t all that long ago that the stocks targeted by the Nobias algorithm for outsized analyst activity were largely the high flying growth stocks with nosebleed valuations. We’ve witnessed a rotation in the market, from growth to value, throughout recent months and it appears that analysts are making that same transition with their coverage. So, with that in mind, let’s take a look at Verizon, a leader in the telecommunications space, largely known for its slow, yet steady growth, and high dividend yield.

Staying true to trend this week, the third company that we’re looking at, Verizon (VZ) is down on a year-to-date basis. This is interesting, because it wasn’t all that long ago that the stocks targeted by the Nobias algorithm for outsized analyst activity were largely the high flying growth stocks with nosebleed valuations. We’ve witnessed a rotation in the market, from growth to value, throughout recent months and it appears that analysts are making that same transition with their coverage. So, with that in mind, let’s take a look at Verizon, a leader in the telecommunications space, largely known for its slow, yet steady growth, and high dividend yield.

VZ shares are down 2.5% year-to-date. Over the trailing 12 months, VZ shares are down 0.5%. During these same two periods of time, the S&P 500 has posted gains of 11.46% and 49.33%, respectively. Without a doubt, VZ has been a laggard. Is this stock a buy after losing so much ground to the major averages over the last year or so? Let’s find out what reputable analysts are saying.

Eric Volkman, a 4-star Nobias analyst who writes for Nasdaq.com recently penned a piece highlighting the company’s first quarter earnings, which were released on Wednesday, April 21, 2021. Volkman began his piece, highlighting the fact that VZ beat analyst expectations on both the top and bottom lines. He said, “For its first quarter of fiscal 2021, the telecom giant managed to increase its revenue by 4% year over year to $32.9 billion. Generally accepted accounting principles (GAAP) net income also headed north, advancing by 25% to $5.38 billion. On a non-GAAP (adjusted) basis, the bottom line profit was $1.31 per share, up from the year-ago quarter's $1.26.”

For the quarter, analysts were expecting $32.47 billion in revenues and adjusted net profits of $1.29/share. Volkman continued, noting that VZ separates its business into three segments: “consumer, business, and media.” He said, “The largest by far -- consumer -- enjoyed nearly 5% growth to $22.8 billion, which the company said was due largely to new phone activations.” Volkman points out that VZ’s business segment posted relatively flat results for the quarter, with sales up just 1%.

VZ’s media segment posted the best growth during Q1, up 10%. However, as Volkman notes, this is the smallest piece of Verizon’s overall business, accounting for just $1.9 billion of the company’s $32.9 billion sales during the quarter. Volkman concluded his analysis, highlighting the forward guidance provided by Verizon during the quarter. He said that Verizon “Believes it will post an adjusted, per-share net profit of $5.00 to $5.15, with service and other revenue growth coming in at 2%. Currently in the midst of rolling out its 5G network, Verizon anticipates its capital spending will total $19.5 billion to $21.5 billion for the year.”

David Van Knapp, another 4-star Nobias analyst who writes for Daily Trade Alert, touched upon these slow growth expectations in an article he recently published, focused around his recent purchase of Verizon shares. Van Knapp says, “Verizon is a high-yield, slow-growth DG [dividend growth] stock. It increases its dividend at only about 2% per year. Some investors would find that unacceptable, but it’s OK with me for a stock yielding >4%. I wouldn’t accept it for, say, a 1%-yielder.” Van Knapp noted that his fair value estimate for VZ shares is $62, meaning that he believes “Verizon is 7% undervalued right now, meaning that its price is, at worst, a fair deal.” He noted that this company might not be appealing to many investors because of its relatively slow growth and slow dividend growth; however, he concludes his article saying, “This purchase is an example of opportunistically investing in excellent companies at attractive prices when they are available. As the entire market is widely considered overvalued, it’s great to find a high-quality company available for a fair price.”

Van Knapp’s fair value estimate is essentially in-line with the consensus fair value estimate by analysts tracked by TipRanks, according to a recent article published by Austin Angelo, a 5-star Nobias analyst writing for analystratings.com. Angelo not only says that the TipRanks consensus is $61.89, but also that J.P. Morgan recently released a note on Verizon, which placed a “buy” rating on the stock with a $64/share fair value estimate. Being that VZ currently trades for $57.30, it appears that shares have upside potential. When reading through these bullish analyst reports, it’s clear that investors view VZ as an income oriented stock. Bullish investors clearly focus on the company’s dividend yield and Verizon’s long history of rewarding shareholders with annual dividend growth.

David Trainer, a 5-star Nobias analyst who writes for Forbes.com, recently published an article titled “Verizon’s Cash Flow Increases The Safety Of Its Dividend Yield”. In his piece, Trainer notes that Verizon “is the featured stock in March’s Safest Dividend Yields Model Portfolio.” Like so many other Verizon bulls, Trainer is willing to take a step back and acknowledge long-term trends when looking at VZ shares, rather than focus too much on the stock’s short-term growth potential.

Both Trainer and Van Knapp discussed the power of compounding when it comes to buying and holding shares of a blue chip dividend growth stock like Verizon. In his piece, Trainer highlighted the company’s long-term profitability metrics, saying, “Verizon has grown revenue by 4% compounded annually and net operating profit after tax (NOPAT) by 5% compounded annually over the past two decades. Verizon’s NOPAT margin increased from 15% in 2016 to 20% in 2020 while its return on invested capital (ROIC) improved from 6% to 8% over the past decade.” Because of this reliable bottom-line growth, Verizon has been able to generate reliable dividend growth as well. Train says, “Verizon has increased its dividend for 14 consecutive years. More recently, the firm increased its dividend payments from $2.29/share in 2016 to $2.49/share in 2020, or 2% compounded annually. The current quarterly dividend, when annualized provides a 4.5% dividend yield.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

Yet, this income oriented focus by management hasn’t come at the cost of capital expenditures (wire-line and wireless networks are very expensive to build and maintain) or making mergers and acquisitions in an attempt to grow sales. Trainer highlights the fact that VZ’s FCF has outpaced its dividend payments over the long-term, saying, “Since 2015, Verizon’s cumulative FCF easily covers it annual dividend payments even after the $3.4 billion spent to acquire Fleetmatics and Telogis in 2016 as well as the $6.4 billion spent to acquire Yahoo, XO Communications.’ fiber business, and fiber optic network assets from WideOpenWest in 2017. Over the past five years, Verizon generated $63.2 billion (27% of current market cap) in FCF while paying $48.8 billion in dividends.”

The major issue that bears have when it comes to VZ stock isn’t the company’s dividend, its business, or its brand name...but instead, the company’s balance sheet. Earlier in 2021, Verizon led all bidders at the FCC spectrum auction, spending more than $45 billion. It appears that the company had to make such a large move to maintain its leadership in the wireless space as competitors launch impressive 5G coverage; however, this heavy spending came at a cost.

Verizon recently surpassed its rival, AT&T (T) as the largest non-financial issuer of debt. During its recent Q1 report, management said, “Verizon's unsecured debt balance increased year over year by $42.9 billion to $147.6 billion in first-quarter 2021, and the company’s net unsecured debt (non-GAAP) increased by $39.7 billion year over year to $137.4 billion.” During the Q1 earnings conference call, Verizon’s CFO, Matthew Ellis, said, “Based on our current cash flow assumptions, we expect our net leverage ratio to be approximately 2.8 times by the end of the year. We will evaluate the level of our cash balance based on the recovery in the economy and developments with the pandemic.”

Although it’s true that Verizon’s cash flows are large, the company’s debt load/net debt ratios are high enough to scare away conservative investors. This is likely to be the story that surrounds VZ shares for years as management attempts to repair the damage that was done to its balance sheet during the recent FCC auction.

Disclosure: Nicholas Ward is long shares of VZ and T. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

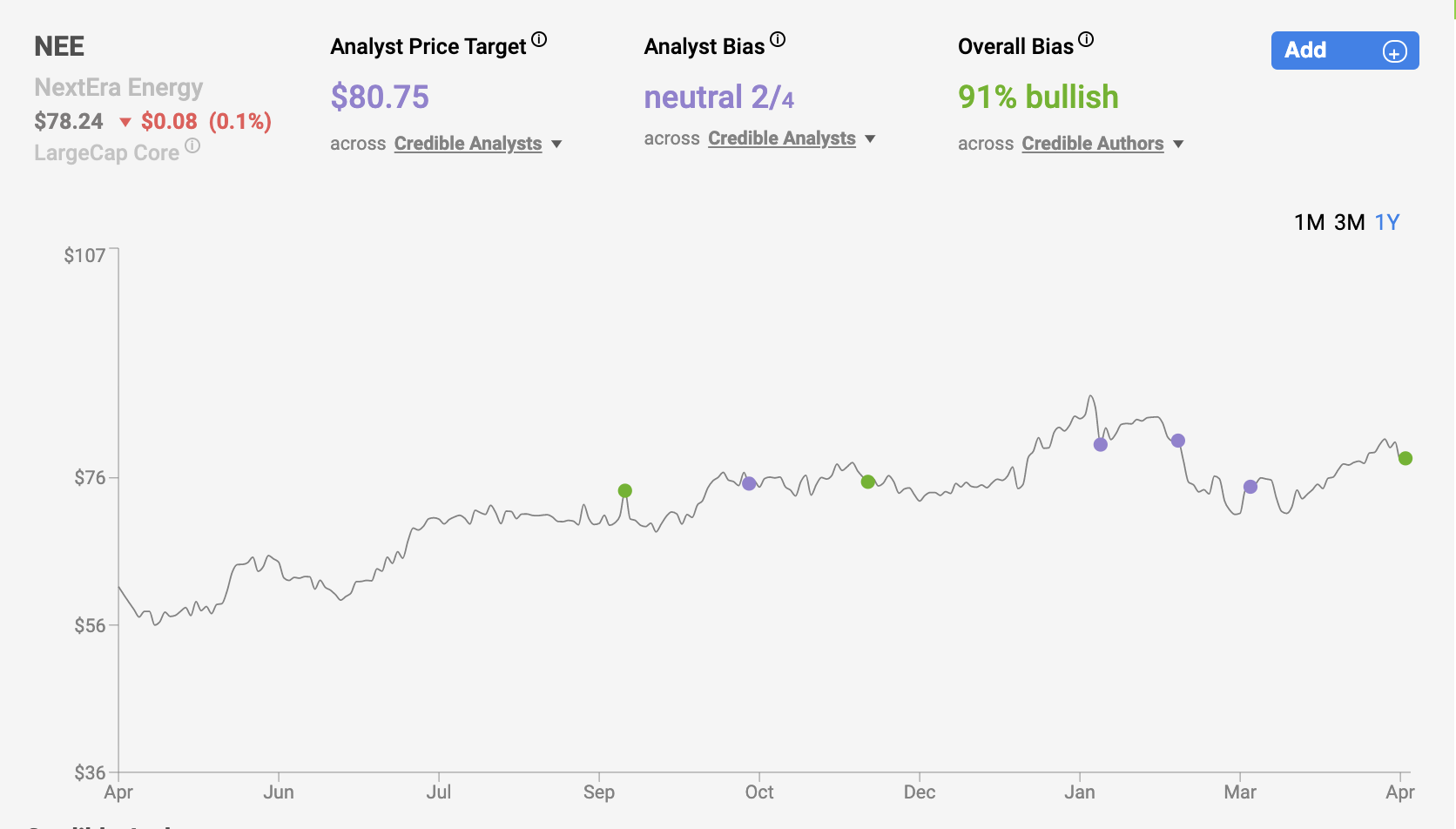

NextEra Energy: Does Future Growth Justify Today’s High Valuation Premium?

Although the transition away from fossil fuels and towards a green energy future seems undeniable at this point in time, many of the stocks in the renewable energy space, which had experienced a strong rally throughout much of 2021 thus far, have begun to experience a sell-off in recent weeks. It’s unclear what caused this sentiment shift. Valuation is likely at play. No equity ever goes up in a straight line, after all. What’s more, the initial exuberance related to the Biden Administration’s major infrastructure spending plans, which involved heavy investments into renewable energy, is beginning to wane.

In recent weeks, it has become clear that compromise is necessary with Republicans, who appear to be much less interested in a “Green New Deal” type of package, for such a large stimulus deal to pass. Furthermore, Republicans appear to be wary of the overall price tag associated with the proposed infrastructure deal, meaning that any deal that makes it through Congress will likely involve much less stimulus and spending than was originally proposed.

Although the transition away from fossil fuels and towards a green energy future seems undeniable at this point in time, many of the stocks in the renewable energy space, which had experienced a strong rally throughout much of 2021 thus far, have begun to experience a sell-off in recent weeks. It’s unclear what caused this sentiment shift. Valuation is likely at play. No equity ever goes up in a straight line, after all. What’s more, the initial exuberance related to the Biden Administration’s major infrastructure spending plans, which involved heavy investments into renewable energy, is beginning to wane.

In recent weeks, it has become clear that compromise is necessary with Republicans, who appear to be much less interested in a “Green New Deal” type of package, for such a large stimulus deal to pass. Furthermore, Republicans appear to be wary of the overall price tag associated with the proposed infrastructure deal, meaning that any deal that makes it through Congress will likely involve much less stimulus and spending than was originally proposed.

What’s interesting is that while trillions of stimulus spending will obviously be bullish for renewable focused names and utility stocks, the green energy movement benefits from secular tailwinds and therefore, even if the stimulus bill never makes it through the halls of Congress and onto Biden’s desk in the Oval Office to sign, it’s very likely that the positive growth trajectory over the long-term in the renewable space remains intact. And with this in mind, we wanted to highlight the recent share price movement of one of the market leaders in renewable energy production, NextEra Energy (NEE), which has been involved in the recent sell-off.

NEE shares are down roughly 3.5% during the past week, pushing their year-to-date returns down to just 1.4%. The S&P 500 is up roughly 11.5% year-to-date thus far, meaning that NEE shares have massively underperformed the broader index. This relative underperformance has led a handful of analysts coming out with bullish opinions in recent weeks.

Right now, when looking at the 4 and 5-star analyst that the Nobias algorithm tracks, we see 6 opinions leaning bullish with just 1 analyst trending bearish with their outlook. With that in mind, it appears that NEE may be an attractive option for investors looking to increase their exposure to renewables. Rekha Khandelwal, a 5-star analyst who writes for The Motley Fool certainly thinks so. She recently penned an article titled, “Is NextEra Energy Stock A Buy?” which offered a strong bullish outlook on the stock. She began her piece by stating that “NextEra Energy has delivered an impressive performance over the years. Its adjusted earnings per share (EPS) grew by 10.5% last year.” This double digit bottom-line growth is rare to find in the utility space, which is generally known for slow and steady revenues and earnings growth. What’s more, Khandelwal notes that NEE’s future growth prospects remain attractive, saying, “The utility expects adjusted EPS to range from $2.40 to $2.54 for 2021, which, at its midpoint, is nearly 7% higher than 2020. Moreover, it expects from 6% to 8% growth in adjusted EPS over the next two years.”

Daniel Foelber, a 4-star analyst who also writes for The Motley Fool, recently wrote an article highlighting his bull case for NextEra, in which he touched upon the company’s operations and stellar past performance. He noted that NEE is best known for its Florida Light and Power Company holdings.

Foelber said, “NextEra's core business is Florida Power & Light (FPL), which is the largest utility in Florida. FPL generates the vast majority of its power from fossil fuels, although it has added renewable capacity, too. FPL's claim to fame is its steady profits and low rates for customers. In a win-win for both NextEra and its customers, FPL's residential customers pay 30% less than the national average.” He continues, mentioning that “NextEra has been using FPL's extra cash and debt to fund its renewable arm, NextEra Energy Resources (NEER).”

Looking at NextEra’s investor relations website, we see that NextEra Energy Resources is “the world's largest generator of renewable energy from the wind and sun and a world leader in battery storage. Through its subsidiaries, NextEra Energy generates clean, emissions-free electricity from seven commercial nuclear power units in Florida, New Hampshire and Wisconsin.”

This combination of reliable earnings from the traditional (and very efficient) utility in Florida and the growth potential of renewables has allowed NEE to post performance well above its peer average over the long-term.

Foelber notes that “Between 2005 and 2020, NextEra grew its adjusted earnings per share (EPS) and dividends per share at compound annual growth rates of 8.7% and 9.6%, respectively.” And circling back to Khandelwal’s piece, we see that the company continues to invest heavily into future growth projects, which create continued strong growth potential moving forward. She said, “NextEra spent $14 billion on capital projects in 2020. The company expects to spend around $44 billion on capital projects through 2025, including nearly $4 billion on wind and solar assets.”

Foelber mentioned the company’s growth plans as well, saying, “To put into perspective the sheer scale of this endeavor, consider that NEER had a renewable capacity of roughly 22 gigawatts (GW) at the end of 2019. After adding 5.8 GW of renewable capacity in 2020, NEER plans on adding an additional 23 GW to 30 GW of capacity by 2024, bringing its total renewable capacity to between 50 GW and 60 GW. Most of NEER's existing and planned renewable capacity is wind energy.”

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

However, there is downside to all of this growth: valuation. Generally speaking, investors are willing to pay higher premiums for stock with reliable growth prospects. However, high premiums do tend to increase risk and lower future return prospects and at a certain point, the valuation gaps between competitors can become so large that the best-in-breed pick in a given sector/industry no longer looks attractive, on a relative basis. For many, this has been the case with NEE in recent years.

Khandelwal notes, “With a forward price-to-earnings ratio of 29, NextEra Energy looks pricey compared to its top utility peers, which are all trading at forward P/E ratios of around 18.” Not only does this price-to-earnings ratio make NEE look expensive relative to its peers, but this ~29x multiple is always well above the company’s own long-term historical averages. NEE’s 5 and 10-year average blended price-to-earnings ratios are 23.5x and 19.8x, respectively. As you can see, there is a clear premium being placed on shares in the present day. However, Khandelwal justifies this, using forward growth, saying, “if we consider NextEra Energy's expected earnings growth, its valuation looks much better. NextEra's forward price-earnings-to-growth or PEG ratio is 0.4 compared to Southern Company's (SO) ratio of 1.4.”

Frankly put, only time will tell if NEE’s growth prospects come to fruition and eventually justify today’s premium. All equities are risk assets and their prices are generally based upon expectations of future cash flows. Investors betting on NEE at roughly 30x earnings are potentially putting outsized risk onto the table. Yet, Khandelwal appears to be comfortable with the risk/reward proposition that NEE shares offer today, saying, “Simply put, a company growing at a higher rate should trade at a higher P/E than another one that is growing at a lower rate, all other things being equal. Generally, a ratio below one indicates that a stock isn't overpriced, based on its expected growth.” And, she concluded her piece with clearly bullish commentary, saying, “NextEra Energy's steady operations combined with its huge renewables portfolio makes it an attractive buy. Its growth plans and outlook inspire confidence in its ability to continue generating peer-leading dividend growth. The stock's recent pullback offers an entry point to build your position for the long term in this top utility.”

Disclosure: Nicholas Ward has no positions in any equity mentioned in this article. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

Will Alibaba Continue to Rally Now That its Anti-Trust Investigation is Over?

Alibaba (BABA) stock is one of the most intriguing tickers in the entire stock market. In the growth space, this is probably the ultimate battleground stock. Bulls will tell you that the company is growing like a weed (which it is; during BABA’s last quarter, its revenue grew by 37% year-over-year and its adjusted EBITDA posted 22% growth). BABA is the eCommerce leader (amongst other things; like its American counterpart, Amazon (AMZN), BABA’s business has expanded away from its eCommerce base into other things like cloud computing, digital payments, logistics, and digital marketing) is Asia, which has a population that can support this immense growth over the long-haul. Unlike Amazon, Alibaba is an asset-light business, which is even more appealing to growth investors who focus primarily on software-as-a-service (SaaS). Alibaba doesn’t own merchandise or warehouses; instead, the company focuses on software solutions that connect buyers and sellers and help goods be delivered in an expedient manner.

Alibaba (BABA) stock is one of the most intriguing tickers in the entire stock market. In the growth space, this is probably the ultimate battleground stock. Bulls will tell you that the company is growing like a weed (which it is; during BABA’s last quarter, its revenue grew by 37% year-over-year and its adjusted EBITDA posted 22% growth). BABA is the eCommerce leader (amongst other things; like its American counterpart, Amazon (AMZN), BABA’s business has expanded away from its eCommerce base into other things like cloud computing, digital payments, logistics, and digital marketing) is Asia, which has a population that can support this immense growth over the long-haul. Unlike Amazon, Alibaba is an asset-light business, which is even more appealing to growth investors who focus primarily on software-as-a-service (SaaS). Alibaba doesn’t own merchandise or warehouses; instead, the company focuses on software solutions that connect buyers and sellers and help goods be delivered in an expedient manner.

The company has exceeded in growing its regional, and even global influence, and therefore, has minted itself one of the premiere technology companies on planet Earth. However, bears will say that none of this growth matters, because frankly, it cannot be trusted. Chinese companies have a long history of shady accounting practices, which have scared off many western investors. What’s more, the threat of regulation from the Chinese Communist Party is a constant threat to growth.

4-star Nobias analyst, Jeremy Bowman of The Motley Fool, recently touched upon his saying, Chinese stocks tend to trade at a discount to their American peers due in part to investor cautiousness about the influence of the Chinese Communist Party.” However, he did go on to note that “the effect of China's anti-monopoly law in this instance isn't much different from that of similar laws in the U.S. and Europe,” pointing towards a potential overreaction.

Lastly, geopolitical disputes between the U.S. and China have recently created another potential headwind for BABA shares: delisting from U.S. stock exchanges. At this point, it’s speculative as to whether or not this threat will come to fruition and if so, which companies would be removed; however, the risk remains a dark shadow above the head of a stock like Alibaba, scaring conservative investors away. But, not all conservative investors. Arguably the king of all conservative, value investors, Charlie Munger, probably best known as Warren Buffett’s right hand man at Berkshire Hathaway, recently initiated a large BABA stake in the Daily Journal’s portfolio, which Munger manages. Alibaba is now the Daily Journal’s third largest holding and this purchase has certainly made waves throughout the value investing community in recent weeks.

Over the last 6 months, BABA shares are down 22.33%. However, during this period, the company’s growth has remained strong. The combination of rising bottom-line results and a falling shares price has resulted in a low price-to-earnings ratio, especially on a forward looking basis. Right now, BABA shares trade for approximately 21.5x their current forward looking consensus estimate for earnings-per-share, which sits at $11.05. This price-to-earnings multiple in the low 20’s means that BABA shares are much cheaper than the popular eCommerce plays. For instance, Amazon shares trade with a forward P/E ratio of 71.1x.

The uncertainty surrounding BABA shares has created an attractive opportunity in the eyes of many investors. We recently tracked reports regarding BABA shares amongst the 4 and 5 star analysts that Nobias follows and saw an average price target of $321.57 (this average was derived from 7 reports posted since the start of 2021). Today, Alibaba shares trade for $238.69, which implies near-term upside of nearly 35%, relative to the 4 and 5 star consensus target.

And, in recent days, the bullish sentiment surrounding BABA has been rising due to what appears to be the conclusion of the anti-monopoly investigation by Chinese regulators that was plaguing the stock. Chinese investigators were looking into Alibaba’s practices of not allowing merchants to sell on other platforms. This investigation came on the heels of the 2020 bombshell news regarding Chinese regulators disallowing the Ant Financial spin-off, which resulted in Alibaba’s famed CEO, Jack Ma, to go into hiding.

The onslaught of regulatory pressure on BABA has been immense; however, when news broke that Alibaba was fined $2.8 billion by the regulators, many viewed this fine as a slap on the wrist. 5-star Nobias analyst, Joe Tenebruso, put this fine into perspective recently, saying, “The penalty payment equates to 4% of Alibaba Group's domestic revenue in 2019. Chinese law allows for a maximum penalty of 10% of revenue. Moreover, there were no requirements for divestitures or major structural changes to Alibaba's business.” While discussing the Alibaba fine in his recent article, Bowman said: “While investors have been fearful of the regulatory grip of the Chinese government, the fine is also notably less than the penalties that Facebook and Alphabet have paid. In 2019, Facebook was fined $5 billion by the Federal Trade Commission over violating consumers' privacy rights, and the stock barely flinched. Alphabet's Google, meanwhile, was forced to pay $9.7 billion in three antitrust cases in the EU.” Bowman continued, noting BABA’s apparent contrition, highlighting a statement that the company offered regarding the fine in which it said, "We are committed to ensuring an operating environment for our merchants and partners that is more open, more equitable, more efficient and more inclusive in sharing the fruits of growth."

As Margaret Moran, a 4-star Nobias analyst who writes for GuruFocus said in her recent article, “Investors cheered the news on Monday, bidding the stock up more than 9% to around $244.01 throughout the day's trading as many were no longer deterred by the uncertainty of pending regulatory concerns.” Moran quoted Alibaba’s Chief Executive, Daniel Zhang, who in response to the regulators’ decision said, “We will incur additional cost. We don't view this as a one-off cost. We view this as a necessary investment to enable our merchants to have a better operation on our platform."

Nicholas Ward is a Senior Investment Analyst at Wide Moat Research. He has spent the last 8 years writing about the stock market at various publications, including Seeking Alpha, The Street, Forbes Real Estate Investor, Sure Dividend, The Dividend Kings, iREIT, Safe High Yield, and The Intelligent Dividend Investor.

These “additional costs” have caused analysts to lower their near-term outlooks for BABA’s bottom-line growth. However, right now the consensus estimate for this year’s earnings-per-share growth remains in the double digits, showing that the regulatory decision is not thought to be crippling, by any means. Moran also noted that Alibaba’s Executive Vice Chairman, Joe Tsai, summed up investor sentiment, saying, "We are pleased that we are able to put this matter behind us." Moran offered a bullish conclusion to her piece, saying, “All things considered – clearing the regulatory hurdle, investing in merchant services, the strength of the company's network effect and the recovery of the Chinese economy, among other factors – Alibaba could be set for a strong run in 2021.”

To conclude his recent Alibaba piece, Tenebruso quoted J.P. Morgan analyst, Alex Yao, who is in agreement with Moran’s sentiment. Yao recently reiterated his overweight stance on BABA shares, noting a $320 price target, which represents roughly or roughly 33% upside, saying, "The event will serve as a closure of investors' concern on Alibaba's core commerce regulatory risks.”

This appears to be the overarching sentiment when it comes to Alibaba shares. The combination of high growth, attractive value, and a reduced regulatory burden, points towards a bullish future. Yet, the threat of heavy handed regulation here remains a threat and only time will tell if this Chinese equity will be able to overcome investor fears related to government oversight over the long-term.

Disclosure: Nicholas Ward is long AMZN but has no position in BABA. Nicholas Ward wrote this article for Nobias at their request with a view of giving investors a balanced perspective based on the writings of Nobias highly rated analysts and bloggers. Nobias has no business relationship with any company whose stock is mentioned in this article and does not have a position in this stock.

Additional disclosure: All content is published and provided as an information source for investors capable of making their own investment decisions. None of the information offered should be construed to be advice or a recommendation that any particular security, portfolio of securities, transaction, or investment strategy is suitable for any specific person. The information offered is impersonal and not tailored to the investment needs of any specific person.

Disclaimer: The Nobias star rating is based on past performance results and is not an indicator of future results. These past performance returns do not represent returns that any investor actually earned. Assumptions made include the ability to purchase the stocks recommended by the author under liquid markets where the transaction would be at the market price for the day. In reality, loss in liquidity may have a material impact on the returns that actually may have been earned. Further, returns are calculated without any including transaction costs, management fees, performance fees or expenses, or reinvestment of dividends and other income. This information is provided for illustrative purposes only.

J.P. Morgan: Can This Big-Bank Maintain Best-in-Breed Status?

J.P. Morgan (JPM) announced its first quarter earnings this week, starting off 2021 with a bang, beating analyst estimates on both the top and bottom lines. JPM’s Q1 revenue came in at $32.3 billion, representing 14.3% year-over-year growth.

During the quarter, the company saw net interest income fall $1.6 billion due to lower rates, but its non-interest revenues rose by $5.7 billion, representing 39% growth. The company’s GAAP earnings-per-share came in at $4.50, beating analyst estimates by $1.38/share. The firm saw its book value per share and its tangible book value per share rise to $82.31 and $66.56, representing 8% and 10% year-over-year growth, respectively. The company returned $7.1 billion to shareholders during Q1; $2.8 billion of which came in the form of a shareholder dividend and $4.3 billion came in the form of net share repurchases.

J.P. Morgan (JPM) announced its first quarter earnings this week, starting off 2021 with a bang, beating analyst estimates on both the top and bottom lines. JPM’s Q1 revenue came in at $32.3 billion, representing 14.3% year-over-year growth.

During the quarter, the company saw net interest income fall $1.6 billion due to lower rates, but its non-interest revenues rose by $5.7 billion, representing 39% growth. The company’s GAAP earnings-per-share came in at $4.50, beating analyst estimates by $1.38/share. The firm saw its book value per share and its tangible book value per share rise to $82.31 and $66.56, representing 8% and 10% year-over-year growth, respectively. The company returned $7.1 billion to shareholders during Q1; $2.8 billion of which came in the form of a shareholder dividend and $4.3 billion came in the form of net share repurchases.